This article provides worked examples for recording the deferred notional gains and reflect the reset cost base for a property if the property has undergone transitional CGT relief in other software before the fund is loaded to Class.

Scenario

A property was acquired by the fund on 19/09/2011 at the price of $1.0 million. The fund has undergone the transitional CGT relief on 30 June 2017 using the proportionate method and the cost base was reset to $1.1 million based on the market value at that time. The amount of the deferred notional gains to be carried forward is $20,000, after applying the discount and pension exemption factor.

The fund is loaded to Class with a book closed date of 30 June 2017 and you are not going to use the depreciation worksheet for the property account.

Example

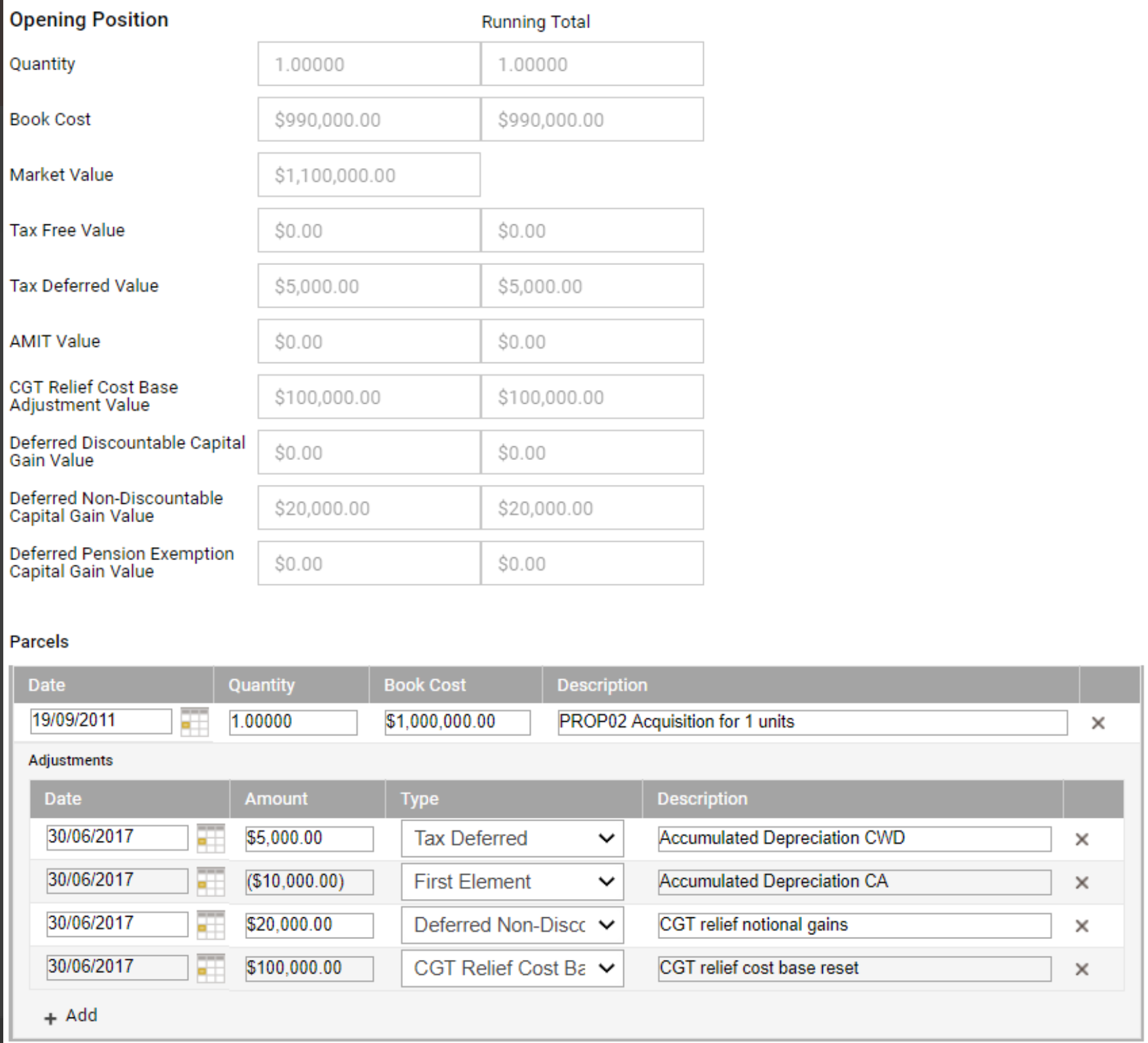

Option 1: Using Edit Parcel History for Investments

Navigate to Fund Level > Load Opening Balances

- Click Edit Parcel History of the property account

- Enter the reset cost base for the property

- Select the 'CGT Relief Cost Base Adjustment' cost base adjustment type

- Enter the differences between the accounting cost base and the reset cost base, i.e. $100,000

- Enter the deferred notional gains

- Select the 'Deferred Non-Discountable Capital Gain' cost base adjustment type

- Enter the $20,000.

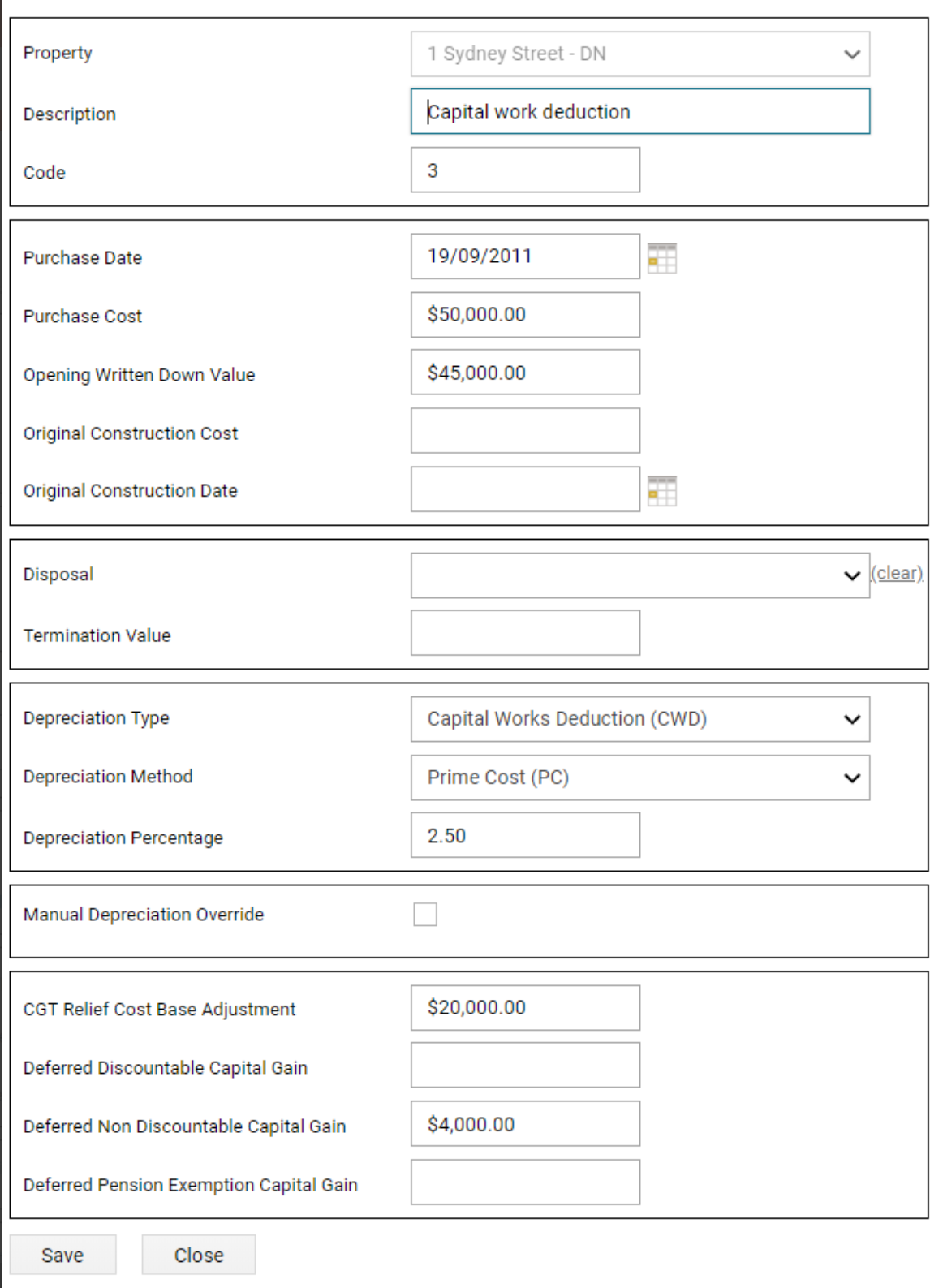

Option 2: Using the Depreciation Worksheet for Property

Navigate to Fund Level > Investments > Depreciation Worksheet

- Select the property account

- Complete the relevant line items in the Depreciation Worksheet

- Enter the deferred notional gains and reset cost base for the portion of the property that attracts CGT

You do not need to record the notional deferred gains or reset cost base for the property account again by Navigating to Fund Level > Load Opening Balances > Maintain Parcel History screen if using the Depreciation Worksheet to take them up.

You may split the notional deferred gains or the reset cost base portion based on each asset if required.

Notional Deferred Gain only applies to non-depreciable assets and Capital works deduction assets in Class

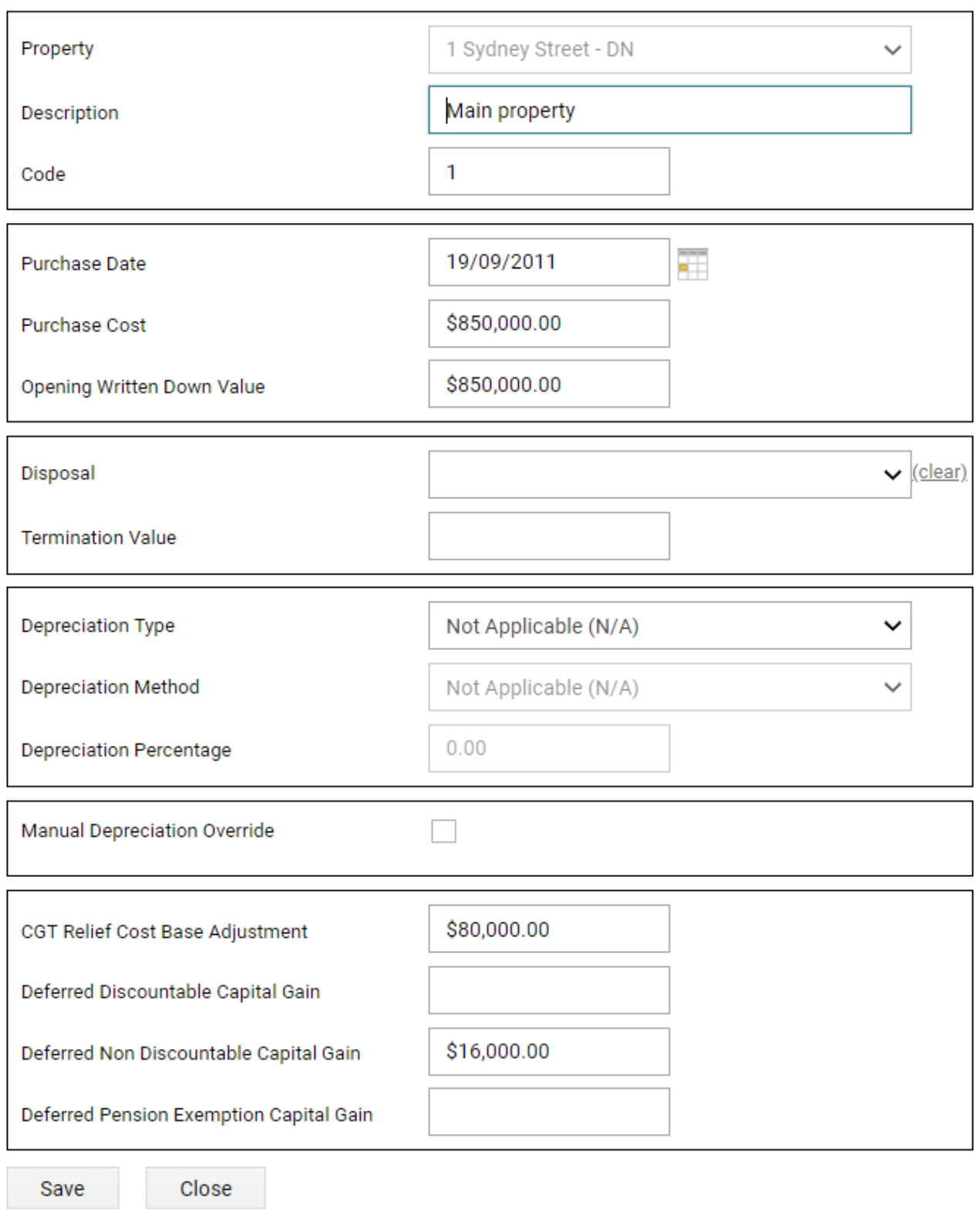

Example of the completed line item for each portion:

The portion which doesn't attract depreciation, e.g. Land.

The portion which attracts capital works deduction, e.g. Building.