Introduction

The Tax Statement event has been updated to cater for Attribution Managed Investment Trust (AMIT) regime. This article explains how to enter AMIT in Class.

Background

From 1 July 2015, an eligible managed investment trusts (MIT) may elect into the new attribution regime for the taxation of MIT. The new tax system is referred to as attribution managed investment trusts (AMITs).

Under the AMIT regime:

- The trust will be treated as a fixed unit trust for income tax purposes

- The trust will be able to attribute amount of taxable income, exempt income, non-assessable non-exempt income, tax offsets and credits to members on a fair and reasonable basis in accordance with their interests, as set out in the constituent documents of the trust.

- If a trust discovers a variance between the amounts actually attributed to members for an income year, and the amounts that should have been attributed, the trust will be able to reconcile the variance in the income year that it is discovered by using the 'unders and overs' regime.

- The cost base adjustment mechanism will be more symmetrical as it provides for both increasing and decreasing adjustments to the cost base of membership interests. If the AMIT cost base net amount is a shortfall, then the CGT cost base of the membership interest will be increased by the AMIT cost base net amount. If the AMIT cost base net amount is an excess, then the CGT cost base of the membership interest will be reduced by the AMIT cost base net amount (but not beyond nil).

|

When assessable and non-assessable |

The AMIT cost base net amount will reflect a: |

Applied to your cost base: |

CGT impact |

|

More than the actual payments (or entitlements) and tax offsets |

Net cost base increase amount |

Increases the cost base and reduced cost base |

Reduced capital gain or increased capital loss on the disposal of the units |

|

Less than the actual payments (or entitlements) and tax offsets |

Net cost base reduction amount |

Reduces the cost base and reduced cost base |

Greater capital gain or reduced capital loss on the disposal of the units |

|

Less than the actual payments (or entitlements) and tax offsets |

Net cost base reduction amount |

If the reduction amount is greater than the cost base amount, it reduces the cost base to nil |

CGT event E10 is triggered – the gross capital gain is the balance of the AMIT cost base net amount |

Worked Example

Background information

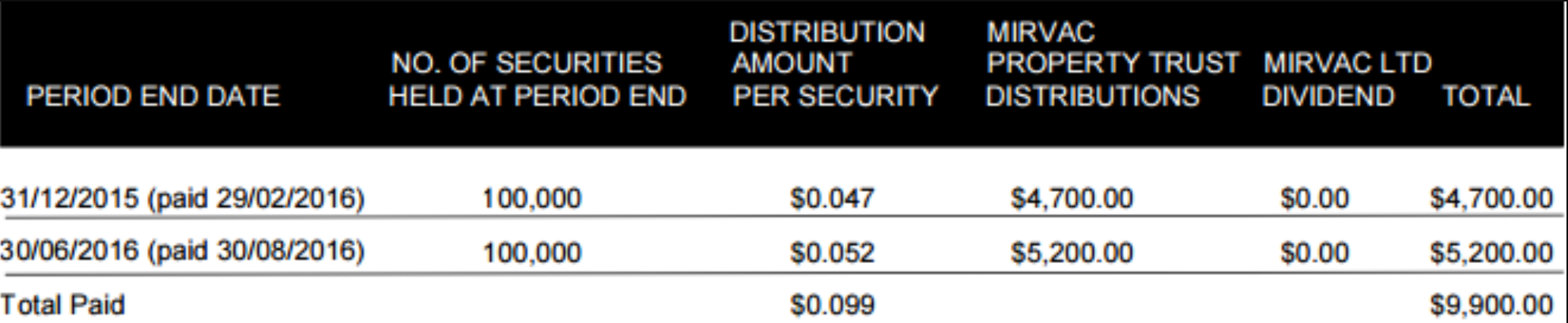

Mirvac Group (MGR) has elected to participate in the AMIT regime for FY2016. 100,000 units of MGR were held for the period 1/7/2015 to 30/6/2016. There are two distributions for the period totaling up to $9,900.

Distribution details

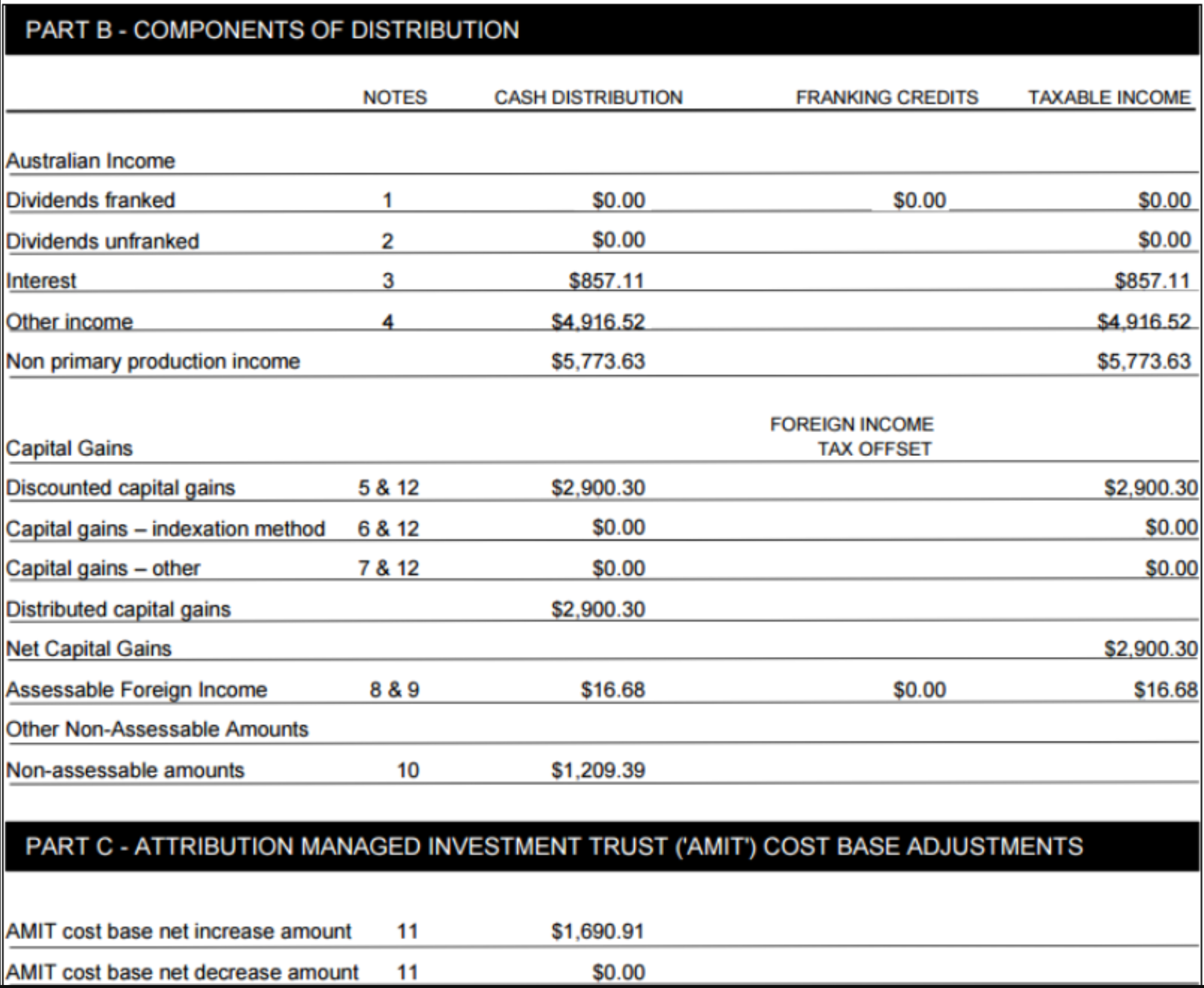

Sample 2016FY tax statement

Completing the Tax Statement in Class

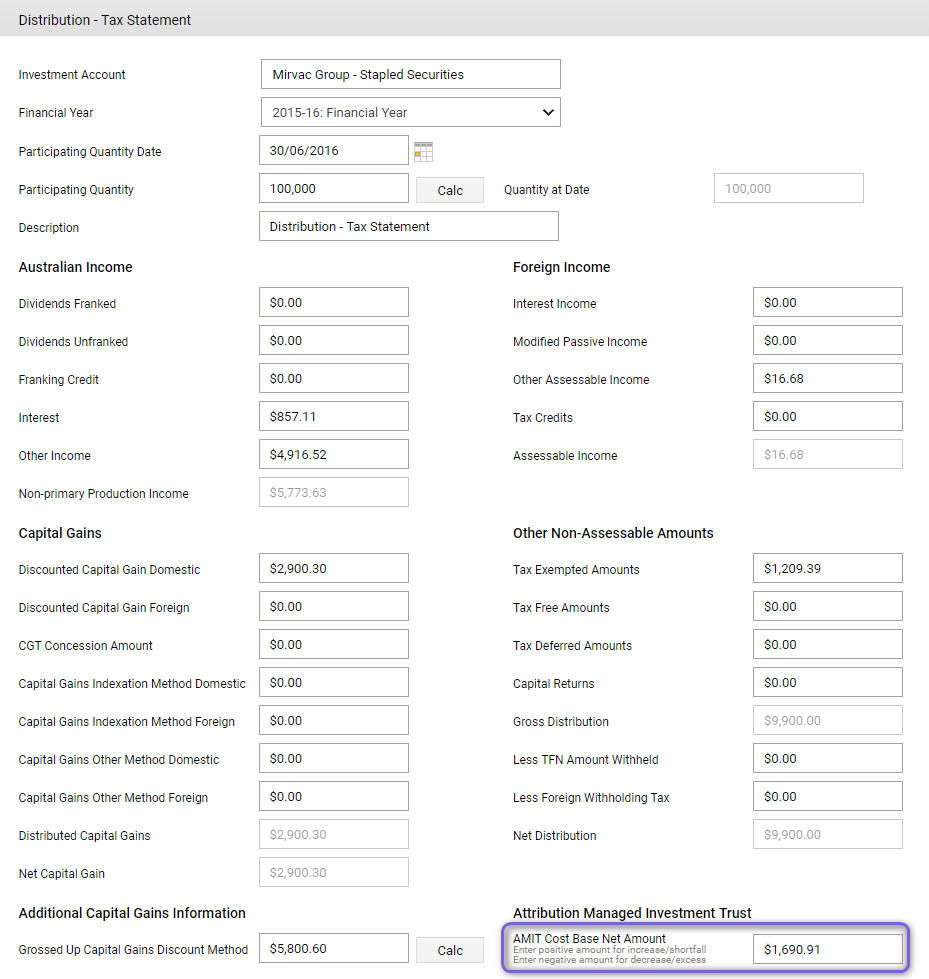

The Tax Statement can be entered as shown below:

Navigate to Fund Level > Transactions > Fund Income > Distribution - Tax Statement

- When there is an AMIT cost base net amount - shortfall, enter a positive amount in the AMIT Cost Base Net Amount field to increase the cost base of the investment.

- When there is an AMIT cost base net amount - excess, enter a negative amount in the AMIT Cost Base Net Amount field to decrease the cost base of the investment.

If the AMIT Cost Base Net Amount field is used, do not use the Tax Free, Tax Deferred Amounts or Capital Returns field in the 'Other Non-Assessable Amounts'. Tax Exempted Amount can still be used as the balancing item with the cash.

Alternatively, in your practice always puts an amount into CGT concession, then the remaining balance should go into Tax Exempted Amount to balance with the cash. By doing this, the Tax Exempted Amount will equal the AMIT amount, but in the opposite direction.