Issue

How to record a distribution - tax statement event in Class when there is a foreign income tax offset attached to capital gain derived from foreign assets, so that:

- Cash is still reconciled; and

- The taxable amount is also reported correctly.

Resolution

The following example demonstrates how to resolve this issue.

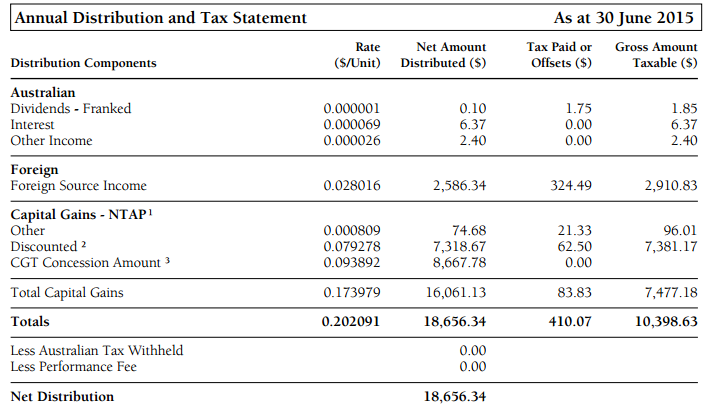

Example Tax Statement

Notes from the Tax Statement:

- Capital gains distributed to non-residents may include both Australian and foreign capital gains; such gains continue to be exempt from Australian tax as they are not in relation to taxable Australian property. These capital gains are therefore labelled above as non-taxable Australian property (NTAP).

- (Australians Only) The amount in the 'Gross Amount Taxable ($)' column needs to be multiplied by two and offset by any capital losses you may choose to apply before applying your appropriate discount concession (ie 50% for individuals and trusts and 33.3% for complying superannuation entities).

- The CGT Concession Amount is the non-taxable amount of the Capital Gain. It may not be the same as the Discounted component because expenses are only allocated against taxable components.

Navigate to Fund Level > Transactions > Fund Income > Distribution - Tax Statement

- Enter the other components from the tax statement as per usual

- Record the Total Foreign Income Tax Offsets (including the portion from foreign capital gains) in the Tax Credit field under foreign income

Tax Credit (Foreign): $408.32 = $324.49 + $83.83 (from Foreign capital gain) - Reduce the Foreign Income by the amount of the Foreign Tax Credit attached to the capital gains

Other Assessable Income (Foreign): $2,502.51 = $2,586.34 - $83.83 - Record the Gross Taxable Amount for Capital Gain derived from foreign asset

Discounted Capital Gain Foreign: $7,381.17

Capital Gain Other Method Foreign: $96.01

- Ensures the Total Foreign Income Tax Offset is captured in the tax statement event.

- Ensures the Gross Taxable Foreign Income (i.e. net foreign income plus foreign tax credits) reported on the SMSF Annual Return agrees with the tax statement. The amount reduced from foreign income in step 2 is added back to the foreign capital gain to ensure the cash is reconciled.

- Ennsures the Grossed Up Capital Gain (Discount Method) is automatically calculated by times 2.