Overview

From 1 July 2017, there are a number of key changes that will affect how exempt current pension income (ECPI) is calculated and applied and whether an actuarial certificate is required by the fund in order to claim ECPI.

What has changed?

1. Transition-to-Retirement Income Streams (TRIS) will no longer receive tax exemption on earnings

From 1 July 2017, SMSFs can only claim ECPI where the current pension liabilities relate to the payment of retirement phase income streams.

This means SMSFs will have to pay tax on the earnings from assets supporting a TRIS where the recipient is under 65 and has not notified the SMSF they have met a condition of release with a nil cashing restriction (retirement, terminal medical condition or permanent incapacity).

2. The eligibility to use segregated method

For the 2017-18 income year onward, SMSFs can no longer use the segregated method to calculate ECPI where at any time during 2017–18 the SMSF had:

- A member with total superannuation balance over $1.6 million immediately before the start of the relevant income year

- That member is receiving an income stream from any source including the SMSF or another super provider.

These SMSF assets are defined as disregarded small fund assets and will not meet the requirement of being 'segregated', even if the SMSF is 100% in pension phase. In this case, the fund may only use the unsegregated method to claim ECPI and must obtain an actuarial certificate.

If the member has any external superannuation interests outside of Class, it is very important to update the external balance information in Class. This information along with the balances in Class will determine if the fund is eligible to apply the segregated method in whole or part of the financial year.

3. New actuarial certificate approach if assets are segregated for part of the financial year

The actuarial certificate now covers only periods where there are unsegregated assets in the fund. For an SMSF that is eligible to use the segregated method in a given financial year, if at any stage during that year there are periods where the assets are solely supporting retirement income streams then those periods are 'deemed' to be segregated.

Earnings received during the deemed segregated period will be fully exempted. For income received outside of the deemed segregated periods, the unsegregated method will be applied to calculate ECPI - assuming the fund hasn't specifically segregated any current pension assets. The actuarial percentage is calculated based on the periods that are not deemed segregated periods and will apply only to income received during the unsegregated periods.

We have summarised the changes of the industry practice as well as from the system's perspective in the table below

|

|

FY 2017 and |

From FY 2018 onwards |

|

Industry Practice |

|

|

|

Fund Policy |

|

|

|

Period Update |

The 30 June period update is required to have the correct actuarial percentage incorporated and will apply the actuarial percentage to the entire financial year |

Period update algorithm has been improved to warn users about boundary condition changes (i.e segregated to unsegregated or vice versa) and/or a conversion of TRIS to retirement phase. Additional data related to both the date and balances will also be included in the actuarial payload when an actuarial certificate is requested |

|

Actuarial Integration |

No changes to existing actuarial certificate processes |

New actuarial payload and certificate process applies from 1 July 2017 |

|

ECPI |

ECPI = (All assessable Income - assessable contribution - non-arm's length income) x actuarial exemption % |

|

|

Capital Gain |

Capital gains are included and form part of ECPI |

Only capital gains derived in unsegregated period are included. |

|

Pension Exemption Fund Expense % |

Incorporating the old ECPI calculation |

Incorporating the new ECPI calculation |

|

SMSF Annual Return |

Unsegregated asset method |

Both segregated and unsegregated assets methods will be selected |

Deemed Segregation – For an SMSF that is eligible to use the segregated method in a given financial year, if at any stage during that year there are periods where the assets are solely supporting retirement income streams then those periods are ‘deemed’ to be segregated.

Deemed Unsegregated – For an SMSF there are periods where it is not in "deemed segregated" during the financial year. This normally implies the fund was either in full accumulation phase or mixed mode where the assets are supporting both accumulation or retirement phase interests.

Worked Example

Case Study Fact:

You are the administrator of Mance Retirement Fund. All the transactions are processed up to 30 June 2018 and you are trying to finalise the fund. Assuming the fund is eligible to use the segregated method.

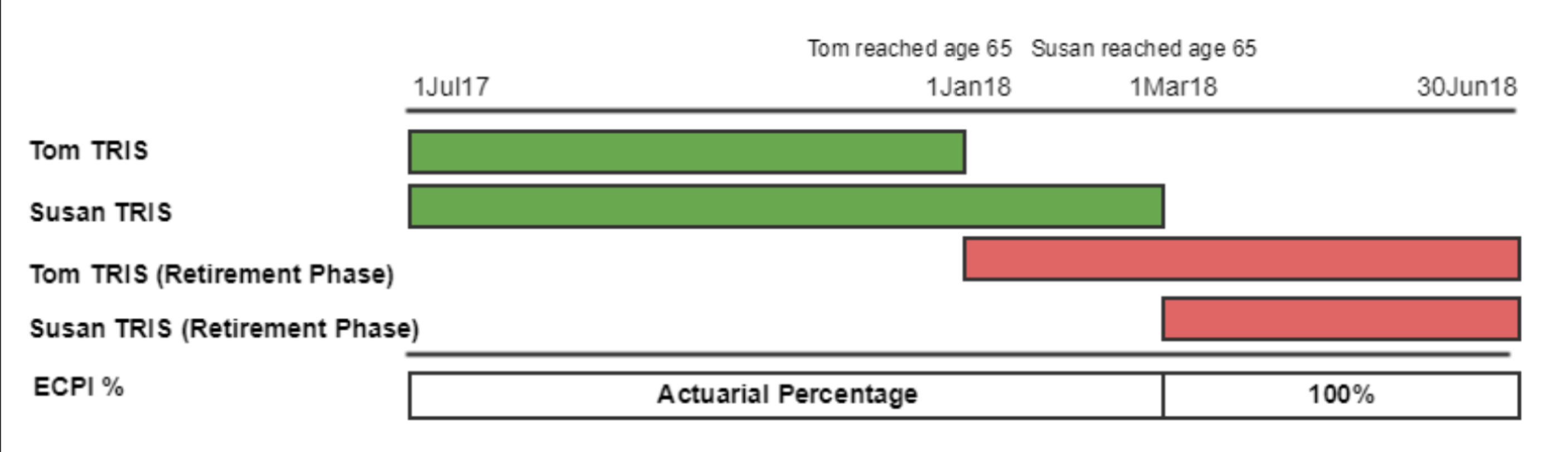

Tom (DOB: 1/1/1953) & Susan (DOB: 1/3/1953) are the only two members of the fund and each of them held a TRIS account as at 1 July 2017. During the 2017/18 financial year, both members have reached age 65 which has converted their TRISs into retirement phase. There are income and expense incurred throughout the period with the actuarial percentage to be 90% for 2017/18 financial year. The fund has switched from unsegregated method to segregated method to calculate ECPI on 1 March 2018.

The fund status throughout the period is summarised in the table below:

|

Period |

Fund Status |

Approach from |

Approach prior to |

|

01/07/2017 |

100% accumulation |

The fund is required to calculate the ECPI on the basis of:

|

|

|

01/01/2018 |

Mixed with accumulation and retirement income streams |

||

|

01/03/2018 |

100% retirement income streams |

|

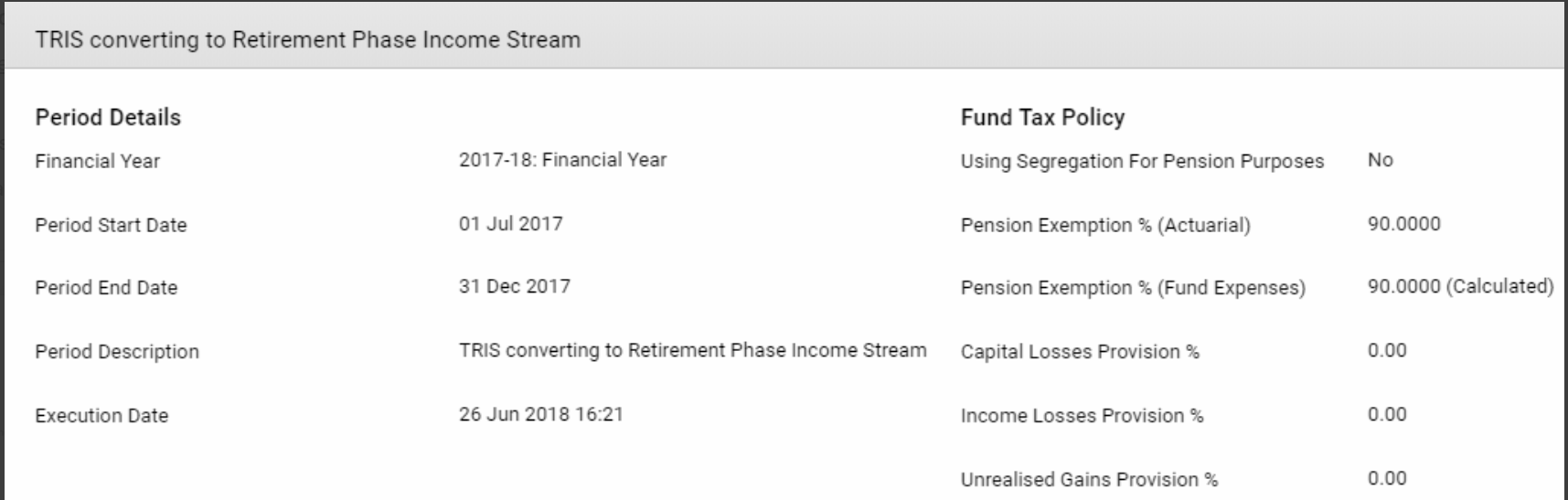

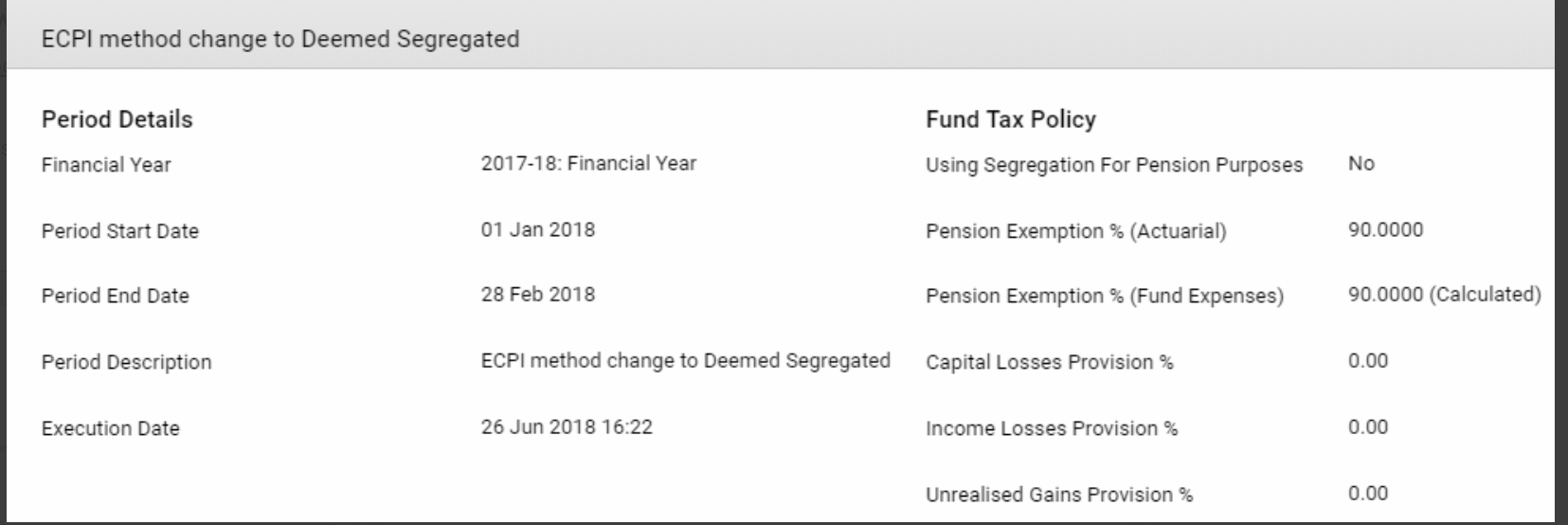

Step 1: Review exception report to identify if any action is required prior to the day the switch of ECPI method boundary conditions or the TRIS conversion happened.

Step 2: Process the period updates in sequence with the earliest date identified above

In the period update processing screen, the Period End Date and the Period Update Description will be pre-filled automatically as the following:

- A day before Tom's 65th birthday

- A day before Susan's 65th birthday - this has also changed the ECPI method for the fund from unsegregated method to deemed segregation from 1 March 2018

Finally, run the 30 June 2018 final period update.

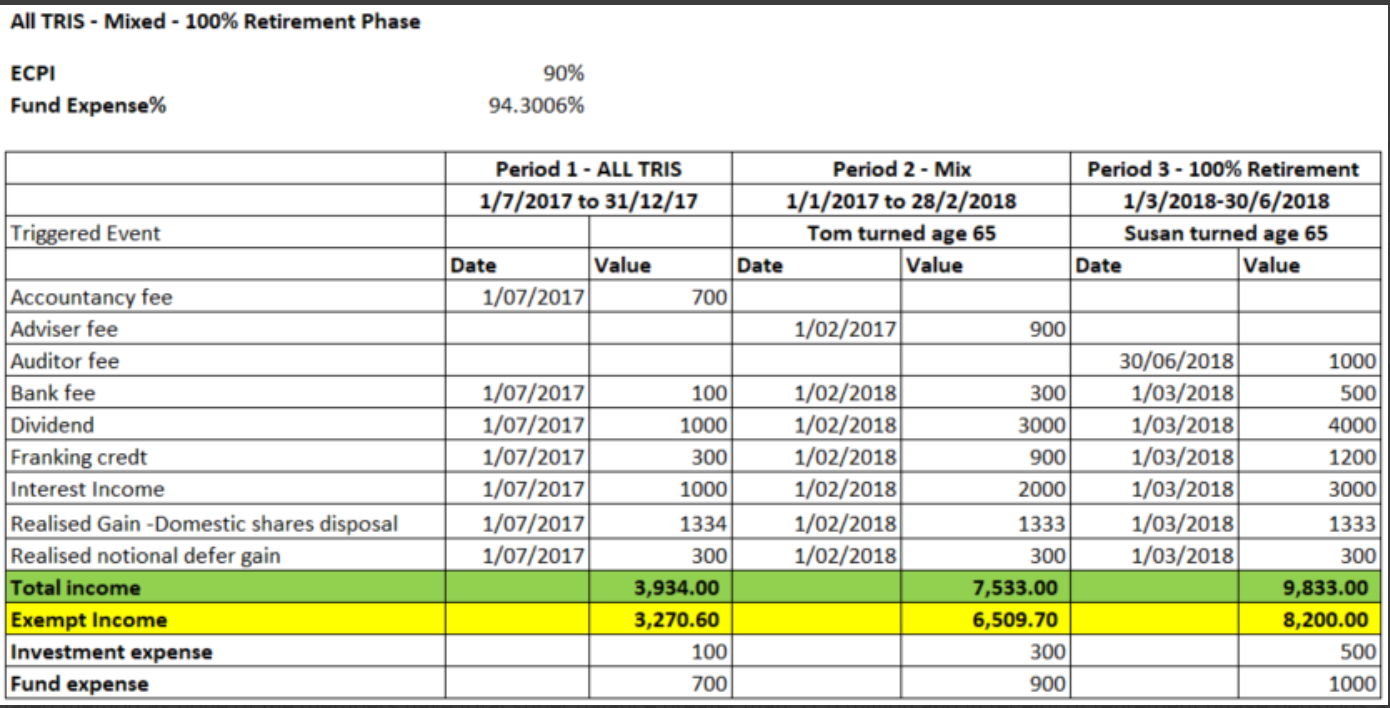

To verify the new TRIS and ECPI approach, we are going to split the income and expense incurred for the three periods, calculate the ECPI for each period then compare the numbers against the Statement of Taxable Income report generated from Class.

Income Expenses Detailed Breakdown

Detailed income and expense breakdown

Comment

- For Period 1 and 2, unsegregated method will be applied. The actuarial percentage of 90% will be applied against the income received (excluding realised notional deferred gains) in those periods to compute the ECPI. The total ECPI for the two period is calculated as: ($3934 - $300) * 90% + ($7533 - $300) * 90% = $9780.30

- For Period 3, segregated method will be applied and all the income (except for realised capital gains and notional deferred gains) derived from this period, will form 100% of the ECPI for this period. Realised gains derived from this period will be completely disregarded. The total ECPI for this period is calculated as: ($9833 - $1333 - $300) = $8200

- Realised notional deferred gain will not be further reduced by actuarial certificate% and the full amount will attract 15% tax

- Fund expense % in this case is calculated by applying the formula:

Exempt Income / (Gross Income - Realised Notional Deferred Gains) = ($3270.6 + $6509.7 + $8200) / ($19,967 - $300*3) = 94.3006%

Unlike the actuarial percentage which will only apply against the period where the fund is not in 100% retirement phase, fund expense % will be applied against the fund level operating expense across the three period to compute the deductible and non-deductible portion of the fund expenses.

In this example, the fund is eligible to use the segregated method as none of the members have total super balance greater than $1.6 million and in receipt of retirement phase pensions as at 30 June 2017, however, say if Tom's total super balance is greater than $1.6 million and is in receipt of retirement phase pensions as at 30 June 2017, the fund will not be eligible to use the segregated method to calculate the ECPI for 2017/18 financial year.

An actuarial certificate is required to be obtained for the entire period even if the assets are solely supporting the retirement pension liabilities for part of whole of the period. The actuarial percentage will be applied to the entire financial year, similar to the approach prior to 1 July 2017.