Overview

The 2019/20 SMSF Annual Return (SAR) stationery has been released by the ATO. Key changes for 2019/20FY SMSF Annual Return include the following areas:

- Section A: Change to auditor qualification question

- Section A: Electronic Fund Transfer > Fund Account Name

- Section C: Remove of anti-detriment/death benefit increase deduction

- Section H: New label for Property Count

- Section K: Minor wording changes to trustee's or director's declaration

- Non-return related SMSF changes

Apart from minor cyclic changes for the financial years, there are no real changes to the CGT schedule and the losses schedule.

2020 SMSF Annual Return Changes

| Annual Return Section | Description |

|

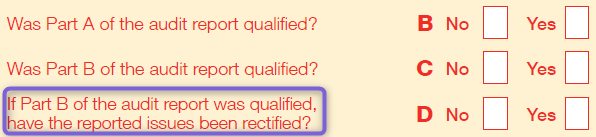

Section A: Fund Information Label 6: SMSF auditor |

Only if Part B of the audit report is qualified, then this question "have the reported issues been rectified?" requires a Yes or No answer. If Part A is qualified, then this question does not need to be updated. However, Part A qualification will be used by the ATO to assess the risk profile of this fund. |

|

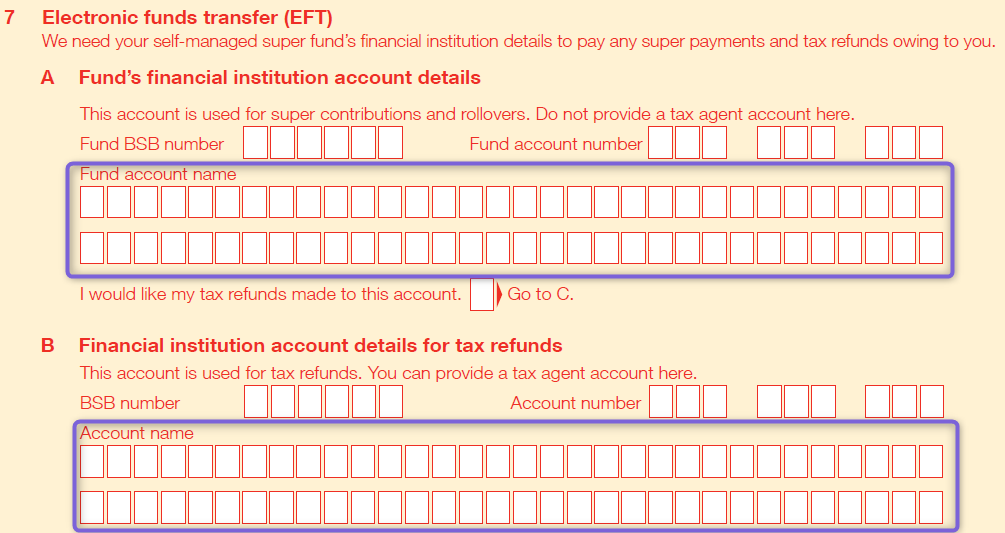

Section A: Fund Information Label 7: Electronic fund transfer (ETF)

|

The ATO has increased the number of characters for the fund bank account name from 32 to 64. This change was introduced in the 2019 SMSF Annual Return, Class has updated them to support both the 2019 and 2020 SMSF Annual Return. |

|

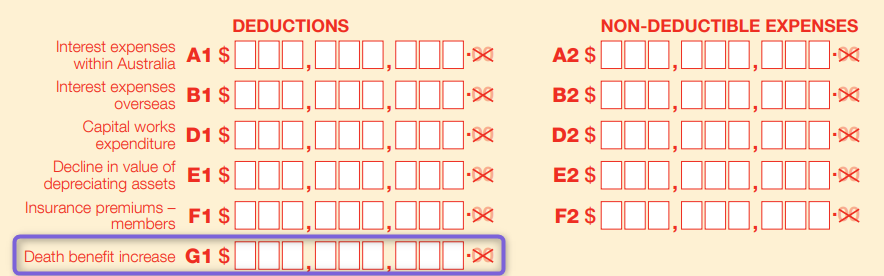

Section C: Deductions and non-deductible expenses Label G1: Death benefit increase

|

Label G1 Death benefit increase at Section C: Deductions and non-deductible expenses has been removed. |

|

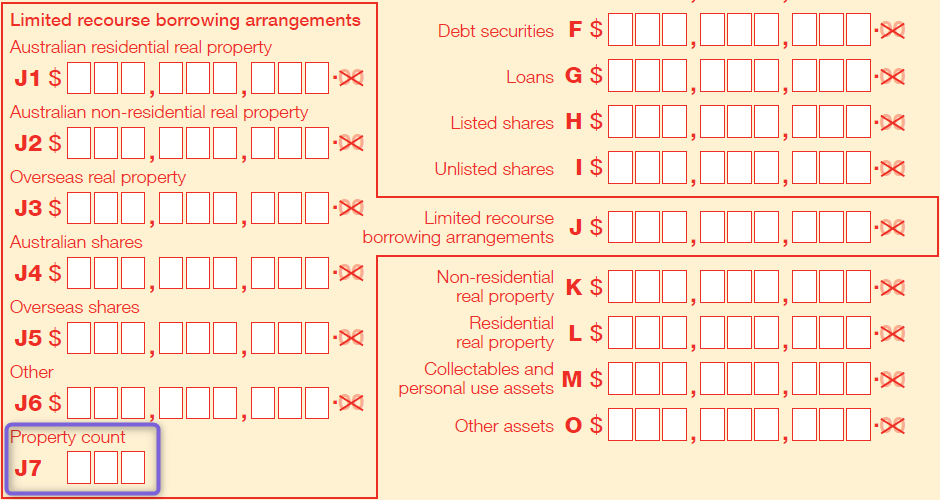

Section H: Assets and liabilities Label J7: Property count

|

A new label J7 Property Count has been added to Section H: Assets and liabilities at Question 15b. If an SMSF holds investments in real property that were held in trust as a security under a limited recourse borrowing arrangement (LRBA), this information must be reported at J7 property count. This label does not apply to properties held directly by the SMSF without LRBA. |

|

Section K: Trustee's or director's declaration

|

Remove the wording (if required) from the "Trustee’s or Director’s Declaration" for 2019/20FY onwards. The ATO has deliberately changed the wording as a reminder that, when a trustee or director of a corporate trustee signs the trustee’s declaration in the return, they confirm that they have received the SMSF independent auditor’s report (IAR) and are aware of any matters it raises. A trustee who signs the return before receiving the IAR could face penalties of up to $12,600 for making a false and misleading statement. |

Non-return related SMSF changes

Broaden the Scope of Non-Arm's Length Income (NALI)

From 1 July 2018, income derived by an SMSF in the capacity of beneficiary of a trust, through holding a fixed entitlement to the income of the trust will be NALI where:

- the SMSF acquired the entitlement under a scheme or the income was derived under a scheme in which parties weren't dealing with each other at arm's length, and

- the SMSF incurred expenses in acquiring the entitlement or deriving the income that is less than, including nil expenses, what the SMSF would otherwise have been expected to incur if the parties were dealing on an arm's length basis. The expenses may be of a revenue or capital nature in the same way that NALI may be statutory or ordinary income.

COVID-19 Related Measures

- Temporary 50% reduction in minimum pension drawdown, and

- Early access of super benefit using the new condition of release "Compassionate Ground - Coronavirus" for members affected by COVID-19.

Lifting the Work Test Age from age of 65 to 67

From 1 July 2020, increasing the age at which the work test applies from 65 to 67, provides an additional opportunity for those who are approaching, or have recently retired, to implement voluntary super contribution strategies over a broader time frame than was previously possible.