Issue

How to treat Retail Premiums on Share Entitlement Offers for Tax Purposes.

Resolution

Where share entitlements are not taken up or not made available for a SMSF, then the correct tax treatment for the fund is to process an Unfranked Dividend or Investment Income (Ordinary Income) rather than Capital Proceeds.

Further information

Commissioner’s View

The ATO’s view on premiums received by a SMSF (as a shareholder) on share entitlement offers is that they should be assessable as unfranked dividends, and if they were not dividends, the retail premiums paid to non-participating shareholders would be ordinary income; instead of capital gains. The summary of the Commissioner’s view can also be found in Taxing Retails Premiums.

The full reasoning behind ATO’s view can be found in the High Court case Commissioner of Taxation v McNeil (2007). Subsequent to this, a Decision Impact Statement was released to provide a statement of the Commission’s position in relation to the decision and how the law will be administered as a consequence of the decision. A Tax Ruling TR 2012/1 was issued to reiterate ATO’s position; however this ruling has limited its application to specific scheme with certain features.

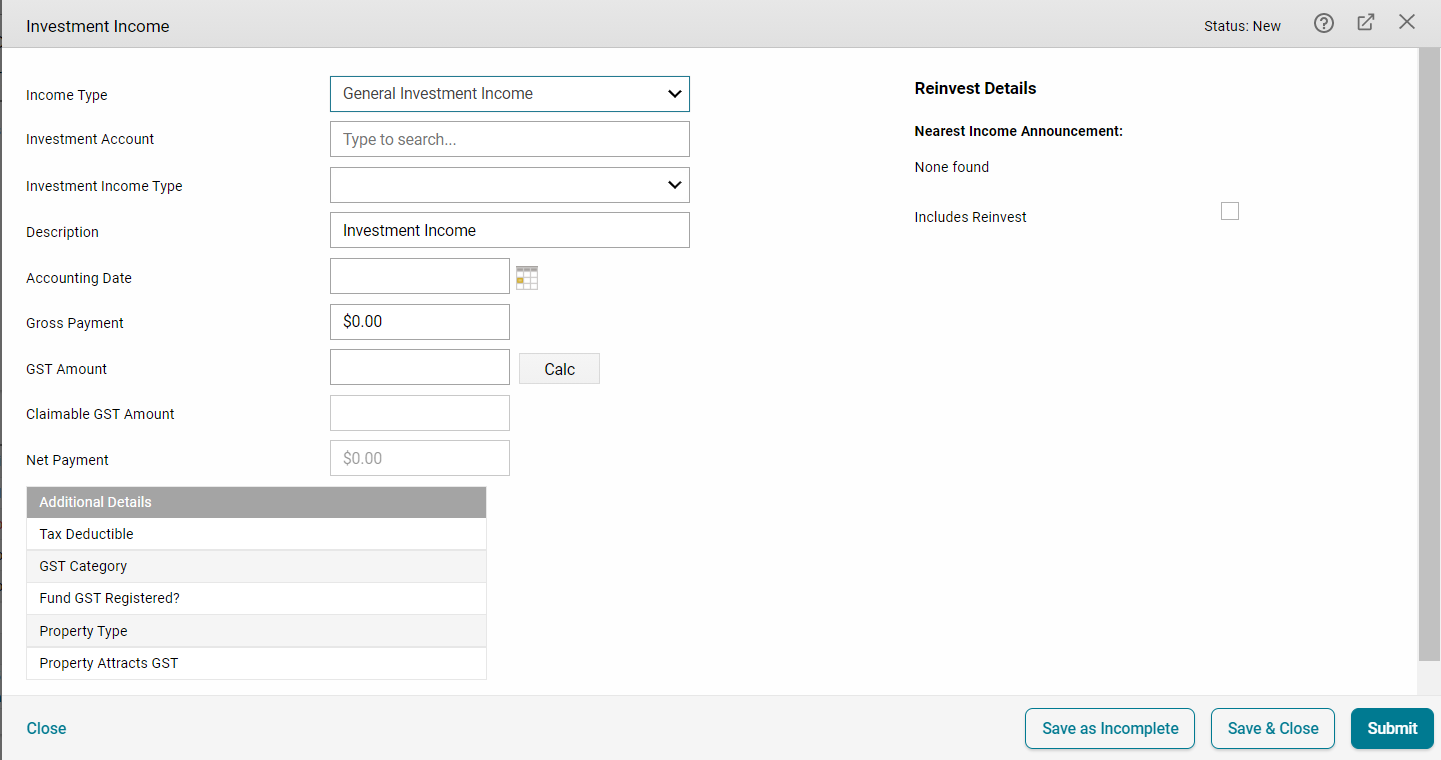

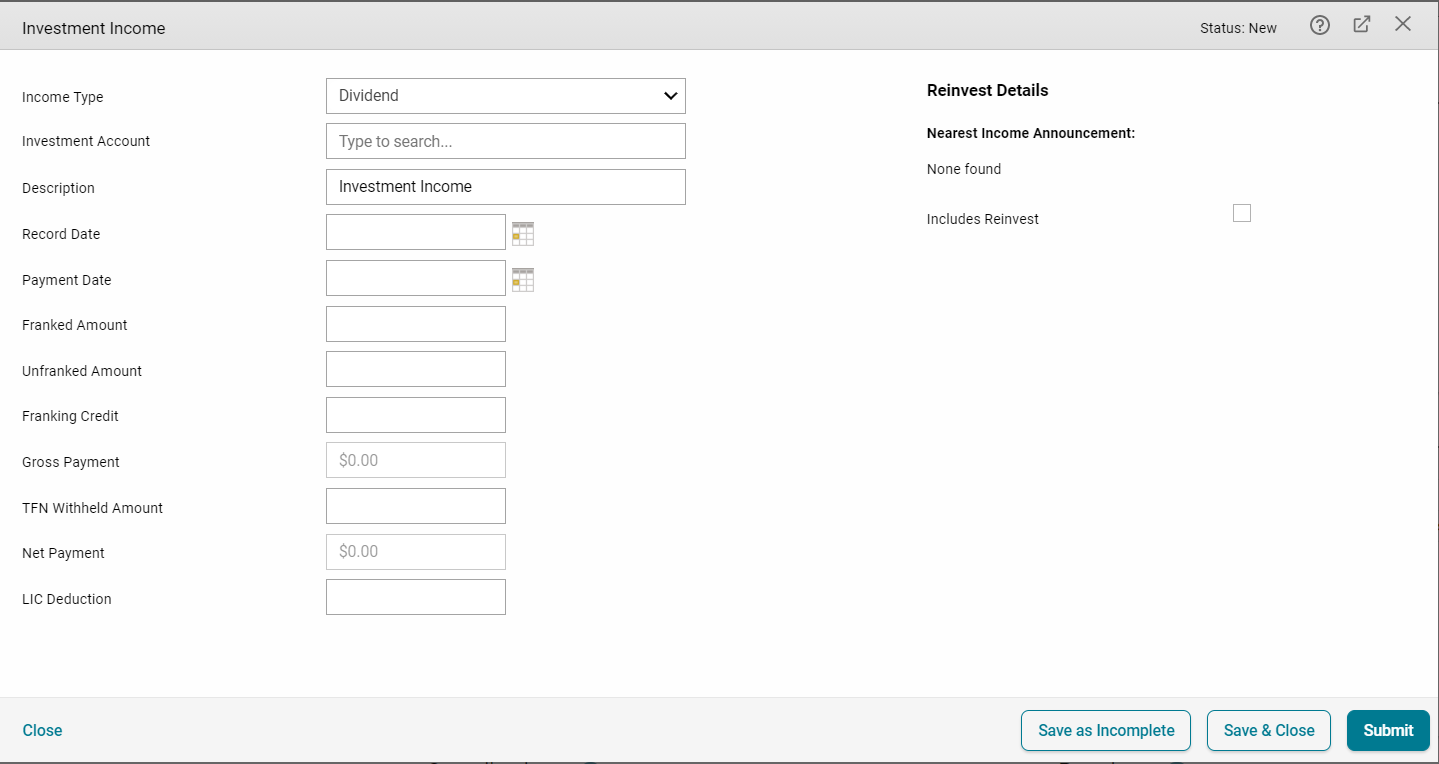

Within Class, these premiums can be processed either as an Unfranked Dividend (under Fund Income) or General Investment Income (under Fund Income) rather than as an Investment Disposal.

Navigate to Fund Level > Transactions > Fund Income > General Investment Income

- Select the Income Type

Other Considerations

Under specific circumstance, there is an argument held by some tax advisers that certain Retail Premium paid to eligible retail shareholders can be treated as capital proceeds if the Retail Entitlements issued are tradable on ASX and they are sold on shareholders’ behalf via the Retail Shortfall Bookbuild. They argue TR 2012/1 is not applicable as this type of capital raising arrangement falls outside scope of the ruling. However, you need to check the specific details of Retail Offer for further information.

Warning: This is a highly contentious area; the ATO may still look to challenge this practice. We strongly recommend you either seek formal determination of ATO’s position based on your specific circumstances through a binding ruling or seek tax advices from qualified professionals.

If you decide to treat the retail premiums received as capital gains, then the rights/entitlement issued should be recorded at original share purchase date for CGT purposes.

Once you have the rights/entitlement created, then you can proceed with the sale of rights for the amount of retain premiums received. Class Super will calculate the correct capital gains and apply discounts to the parcels where applicable.

Disclaimer

Any information expressed in this article does not purport to be any financial or tax advice as we have not taken into account any of your financial or tax objectives that are specific to your circumstance. Additionally, each corporate action may have specific details that mean that their treatment is materially different to what is stated for the general case covered in this document. While effort has been exerted to make sure the information is as accurate and relevant as possible, it is general information on how to use the Class Super software. You should not rely on the information provided as advice, instead seek your own independent advice from appropriately qualified practitioners or conduct your own research.