Overview

Transitional CGT relief is temporary relief available to super funds for certain CGT assets that will lose the tax exemption in complying with the Transfer Balance Cap Reporting (for Retirement Phase Income Streams) (TBC) and transition to retirement (TRIS) changes. The CGT relief allows trustees to elect to reset the cost base of assets that will no longer be eligible to support retirement phase income streams from 1 July 2017 to their market value.

To be eligible for the CGT relief, the asset must have been held throughout the pre-commencement period, from 9 November 2016 to 30 June 2017.

How CGT relief applies

The mechanism used to reset the cost base of a CGT asset to its market value is to deem a sale followed by an immediate repurchase of the asset. The CGT discount period is also reset. The capital gain or loss arising at this time will be entirely disregarded for funds using the segregated method, or for funds using the unsegregated method, partly disregarded and may be deferred . The CGT relief is only optional and may be applied on an asset-by-asset basis.

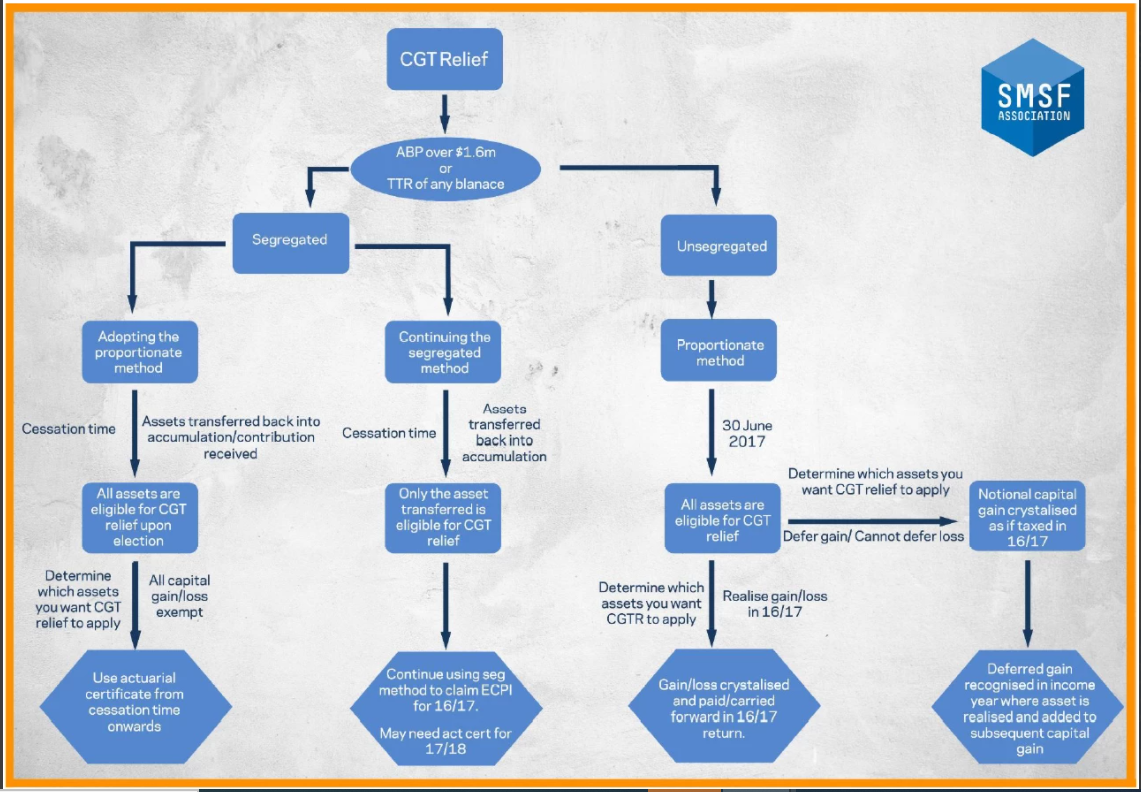

CGT relief will apply differently depending on whether the exempt current pension income (ECPI) is calculated using the segregated method or proportionate method for the year.

- Segregated method - select specific assets to support the income streams

- Proportionate method - allocate a percentage of the total assets to support the income streams

CGT relief using the proportionate method

If you have been using the proportionate method and continue to use it throughout the pre-commencement period, CGT relief is available for all the assets. Capital gains that arise when resetting the cost base for unsegregated assets may be partly disregarded and may be deferred until the asset is sold.

- The acquisition date for the asset will be reset to 30 June 2017

- The reset cost base will be the assets' market value on 30 June 2017

CGT relief using the segregated method

If you have been using the segregated method and either continue to use it, or switch to the proportionate method, an asset must cease being a segregated current pension asset during the pre-commencement period to be eligible for relief. The capital gain or loss for that asset will then be entirely disregarded.

- The acquisition date for the asset will be reset to the cessation time

- The reset cost base will be the assets' market value on the cessation time

Cessation time: At a time during the pre-commencement period, the asset ceases to be a segregated current pension asset. This time is referred to as the 'cessation time'.

Practically, this means when the asset is transferred out of the pool of segregated current pension assets back into accumulation, or you make and record an election to switch to the proportionate method.

If there are investments that have a partial sale between 09/11/2016 and 30/06/2017, refer to How to process partial sales before 30 June 2017 but after CGT relief event for segregated funds for additional steps before processing this event.

Additional Reference

SMSF Association has provided a detailed flowchart (see below) on how CGT Relief can be applied.

CGT relief does not apply automatically. It requires the trustee to notify the ATO in an approved form (i.e. the CGT schedule) on or before the day the fund is required to lodge its 2016-17 tax return. The choice is irrevocable once the form is lodged.

Changes Class made to accommodate this change

|

Changes |

Description |

|

Capital gain relief analysis reports |

Class has two reports: _Capital Gain Relief Analysis - Segregated and Capital Gain Relief Analysis - Proportionate to allow you to identify a list of investments at parcel level which may potentially take advantage of this transitional CGT relief. |

|

CGT relief application event |

CGT Relief Application event is available in Class to allow you to make elections to the list of investments to undertake this CGT relief at the parcel level. The deferred capital gain can then be reported correctly when the CGT assets are eventually sold. |

|

CGT relief application minute |

The CGT Relief Application Minute is available in Class to document the assets that were selected to apply the CGT relief to comply with the reporting and record keeping obligation. |

|

Annual return and CGT schedule |

SMSF annual return and CGT schedule have been updated to specify the total relief to apply. |

Further reading

- Law Companion Guidelines (Final): LCG 2016/8: Superannuation reform: transfer balance cap and transition-to-retirement reforms: transitional CGT relief for superannuation funds

- Guidance Note 6: Transitional CGT relief

- ATO Website (FAQ): Whether an actuarial certificate is required if the SMSFs cease to be segregated before 1 July 2017 (Search for keyword 'actuarial certificate' within the page)

- SMSF Association: Go-To Guide CGT relief (restricted to site members)