This article explains how Traditional Securities are set up in Class, what they are and how they are treated when gains or losses are derived from their disposal.

Background

What is a Traditional Security?

A Traditional Security is broadly, a security (typically bonds, debentures, bills of exchange, promissory notes, loans and deposits with banks, building societies and other financial institutions) that is:

- Not issued at a discount of more than 1.5% multiplied by the number of years in the term of the security

- Does not bear deferred interest

- Is not capital indexed.

Shares in companies and units in managed funds are generally not Traditional Securities.

How are the Gains or Losses treated for Traditional Securities?

Gains on Traditional Securities issued after 10 May 1989 are taxed as ordinary income (s.26BB of ITAA 1936). Gains are treated as the difference between the payment received on disposal or redemption less the cost of the security. Unlike the taxation of capital gains, no indexing or discount is applied.

A loss on the disposal or redemption of a Traditional Security is deductible in the income year in which the disposal or redemption takes place, provided the loss was incurred in the normal course of trading on a securities market.

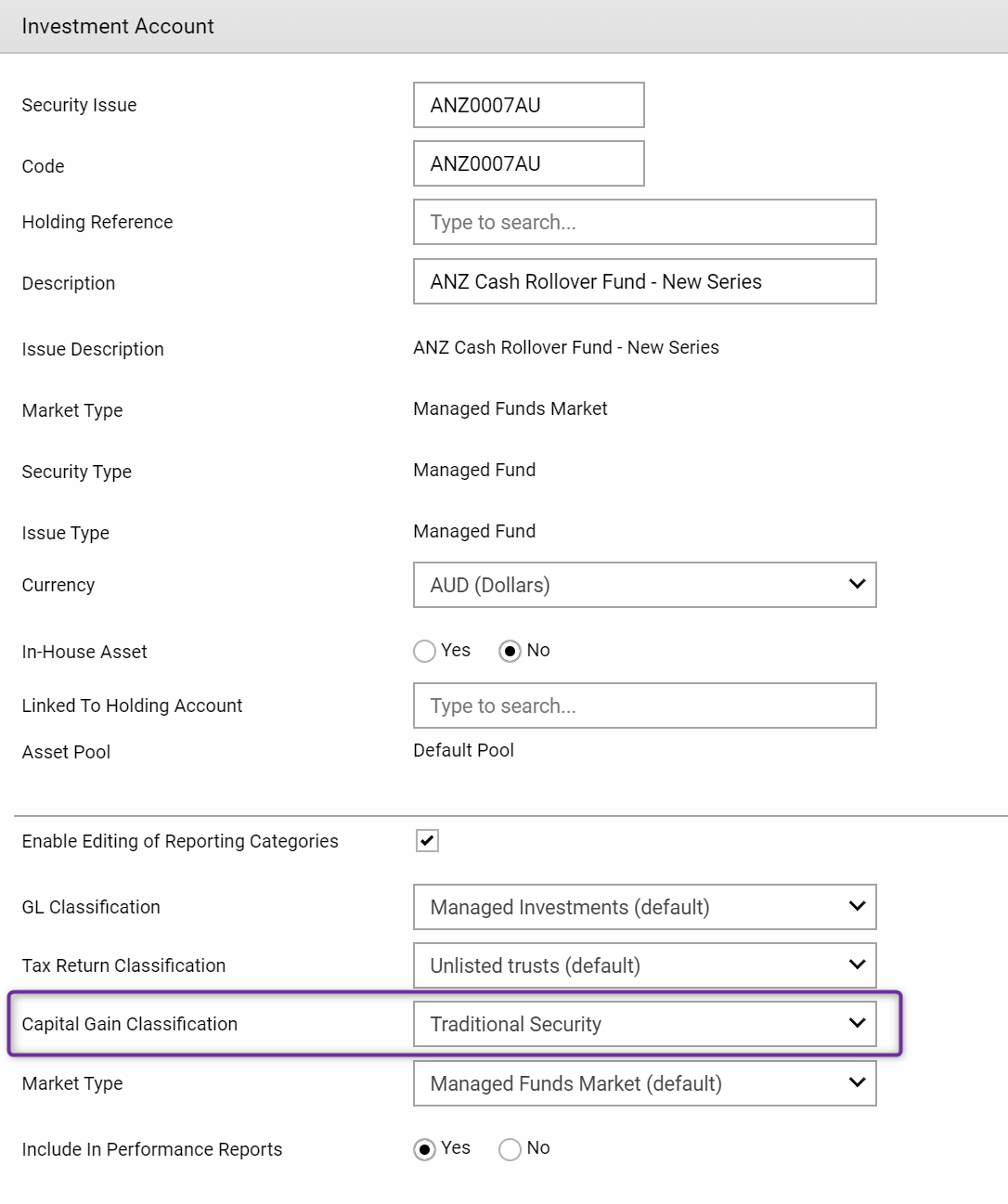

How to set up a Traditional Security

Class Super does not assume whether a security is a Traditional Security or not. You have to set up a security as normal Listed Securities, Managed Funds, Unlisted Securities or Money Market Securities. It must be done through Investment Account.

Once you have set up the Traditional Security as a Security, you can change the Capital Gain Classification to "Traditional Security". By changing the Capital Gain Classification to Traditional Security, Class no longer treats the security, when it is disposed of, for CGT purposes, rather it will show as other gains or losses.

Financial Report

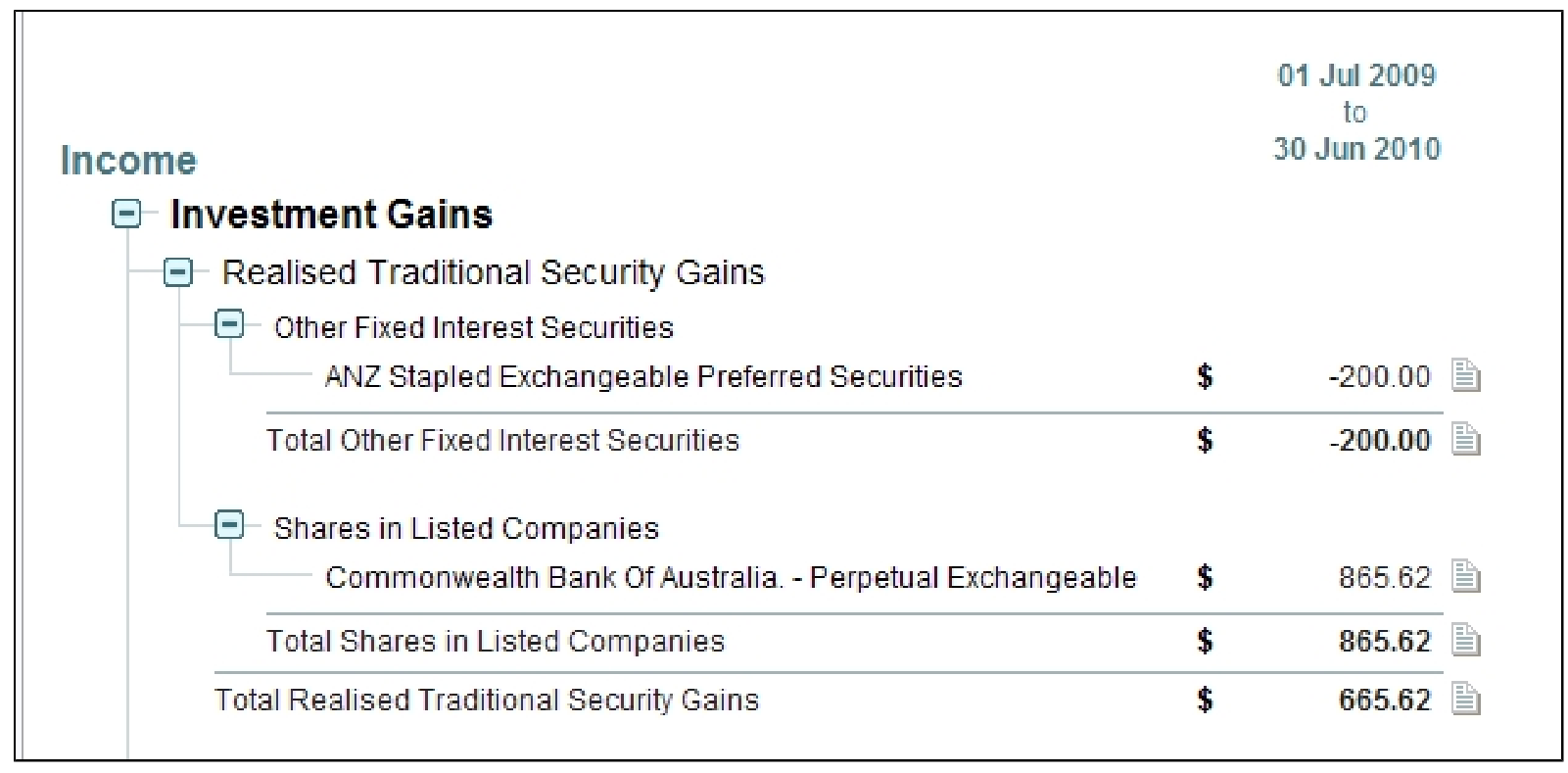

There is a new General Ledger account on the Operating Statement, called Realised Traditional Securities Gains / Losses to record any gains or losses generated when the Traditional Securities are redeemed or disposed of.

Annual Tax Return

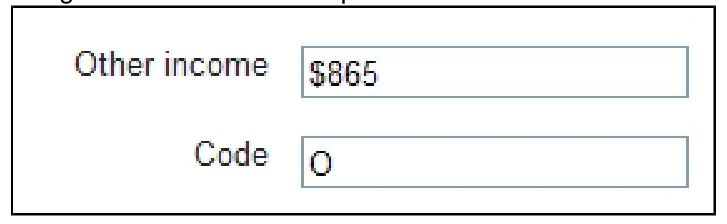

The gains derived on the disposal of Traditional Securities will be classified as Other Income under Section B Income, Label S Other Income.

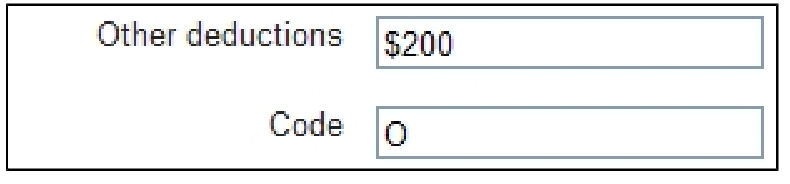

The losses incurred on the disposal of Traditional Securities will be classified as Other Deductions under Section C Deductions, Label M Other Deductions.