This page explains how you can identify complying/term allocated pensions in Class and how to work out and record the 'special value' of these accounts to be counted towards the transfer balance cap.

This page is for general information only without taking into account particular objectives, financial circumstances, and needs. Before making any decision based on this information, you should assess its relevance to the individual circumstances of your client. You may wish to seek your own independent advice from an appropriately qualified professional or conduct your own research.

Background

The transfer balance cap rule limits the maximum amount a member can transfer or retain in the retirement phase superannuation interests. However, the rule applies differently where the member is in receipt of certain capped defined benefit income streams (CDBIS) because amounts can't generally be removed from these income streams through commutation.

Capped defined benefit income streams include:

- certain lifetime pensions, regardless of when they start

- certain lifetime annuities that exist prior to 1 July 2017

- certain life expectancy pensions and annuities that exist prior to 1 July 2017

- certain market-linked pensions and annuities that exist prior to 1 July 2017

When the member has a CDBIS, you will need to work out the 'special value' of the income stream. This value will count towards the member's transfer balance cap. It gives rise to a credit in the member's transfer balance account on the date the income stream first becomes payable to the member where this date occurs on or after 1 July 2017. The way to calculate the 'special value' is covered in the following sections.

Identifying the pension accounts

A new filter has been added to the member console to assist you in identifying those complying / term allocated pensions accounts.

Navigate to the Member console > Select Financial Year 2016-17 > Click on Filter > Select Complying / Term Allocated.

It should show the existing Complying / Term Allocated accounts that have a balance.

If the list comes up blank, it means there are no complying or term allocated pension balances within your business as at 30 June 2017, therefore, no further action is required. Term allocated pensions are often known as market-linked pensions.

Pension Types

| Common Pension Products | Class Pensions | Ceased Date | TBAR Value |

|---|---|---|---|

| Account Based Pensions | Account Based | Active | Closing Balance / Purchase Price |

| Transition to Retirement Income Streams | Account Based (TRIS*) | Active | N/A |

| Allocated Pensions | Allocated Pension | 30 Jun 2007** | Closing Balance |

| Transition to Retirement Allocated | Non Commutable Allocated Pension | 30 Jun 2007** | Closing Balance |

| Lifetime Pensions | Complying | 31-Dec-05 | Special Value |

| Life Expectancy Pensions | Complying | 31-Dec-05 | Special Value |

| Fixed Term Pensions | Complying | 31-Dec-05 | Special Value |

| Flexi Pensions | Flexi | 31-Dec-05 | Special Value*** |

| Market Linked Pensions | Term Allocated Pension (TAP) (commence date before 1 July 2017) | 30 Jun 2007** | Special Value |

| Market Linked Pensions | Term Allocated Pension (TAP) (commence date on or after 1 July 2017) | Active | Purchase Price |

* Existing TRIS, any subsequent establishment or commutation of TRIS is excluded from TBAR reporting purposes. However when TRIS converts into a Retirement Phase Income Stream, it becomes a reportable event, there will be separate workflow to capture the reporting of TRIS conversion for TBAR purposes.

** There are transitional measures in place for pensions created between 30 June 2007 and 19 September 2007

*** For flexi pensions, the TBAR value is worked out using the method set out in r.307-205.02(2) of the Income Tax Assessment Regulations (ITAR) 1997, not 30 June 2017 closing balance.

Calculating the 'special value'

| Product | Pension Type in Class | Calculation Steps | Example |

|---|---|---|---|

| Lifetime pension SISR 1.06(2) | Complying Pension | 1. Work out the annual entitlement | David needs to work out the special value of his lifetime complying pension. The special value of his lifetime pension at 1 July 2017 is 16 times his annual entitlement for 2017–18. |

| Lifetime annuity SISR 1.05(2) | The first fortnightly payment after 1 July 2017 is $5,753.42. | ||

| Other CDBIS as identified by the law | Annual entitlement = First payment / Days in period * 365 |

1. David's annual entitlement is worked out as follows: $5,753.42 / 14 * 365 = $149,999.88 |

|

| 2. Special Value = Annual entitlement * 16 |

2. The special value is then worked out by multiplying his annual entitlement by 16: $149,999.88 * 16 = $2,399,998.08 |

The special value of David's lifetime pension is $2,399,998.08 and a credit will arise in his transfer balance account on 1 July 2017 equal to this amount.

Although David exceeds his transfer balance cap of $1.6 million, because the excess is solely from a capped defined benefit income stream, he does not have an excess transfer balance. As David's benefits exceed his defined benefit income cap ($100,000 for 2017–18), 50% of the excess (i.e. $25,000) may need to include amounts in his assessable income. His entitlement to a tax offset may also be affected.

| Product | Pension Type in Class | Calculation Steps | Example |

|---|---|---|---|

| Life expectancy pension SISR 1.06(7) | Complying Pension | 1. Work out the annual entitlement * Annual entitlement = First payment / Days in period * 365 | Just before 1 July 2017, Victoria has a market linked pension. The first benefit she is entitled to receive from her pension just after that time is her fortnightly payment of $2,301.37 due on 4 July 2017. The current account balance of the pension is $550,000 and remaining term in Victoria's pension just before 1 July 2017 is 9.75 years |

| Life expectancy annuity SISR 1.05(9) | Complying Pension | 1. Work out the annual entitlement | 1. Victoria's annual entitlement just before 1 July 2017 is worked out as follows: First payment / Days in period * 365 = 2,301.37 / 14 * 365 = $60,000 |

| Market linked pension SISR 1.06(8) | Complying Pension | 2. Special Value = Annual entitlement * number of years remaining (rounded up to the nearest full year) | 2. The remaining term in Victoria's pension account is rounded up from 9.75 years to 10 years when determining the pension's special value. |

| Market linked annuity SISR 1.05(10) | Complying Pension | 2. Special Value = Annual entitlement | 3. The special value of Victoria's pension just before 1 July 2017 is calculated as follows: $60,000 * 10 = $600,000 |

| Market linked pension (RSA) 1.07(3A | Complying Pension | 2. Special Value = Annual entitlement | 4. Note that when calculating Victoria's total super balance, her pension will be valued as $550,000. |

If the member only receives capped defined benefit income streams (and has no other retirement phase interests), the balance of the transfer balance account can never exceed the capped defined benefit balance. This applies regardless of whether the special value of the capped defined benefit income stream exceeds the member's transfer balance cap. This means the member will not have an excess transfer balance.

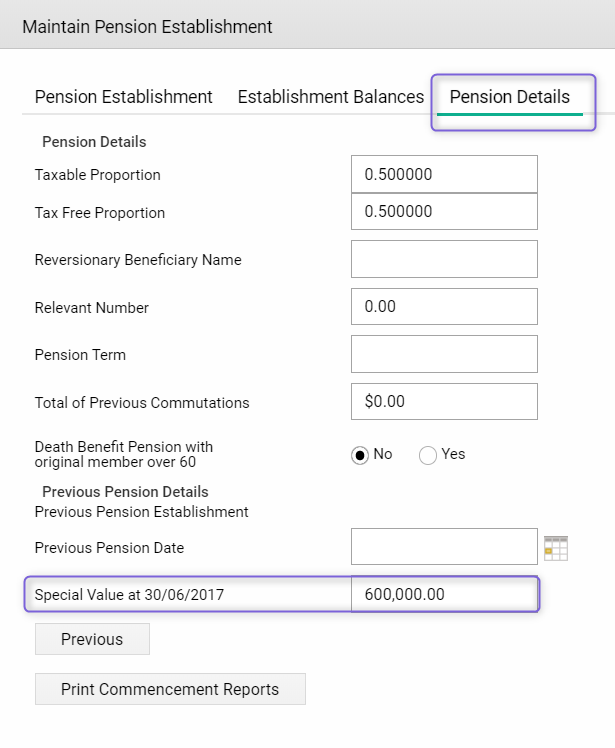

Entering the 'special value'

There is a field for you to record the special value as at 30/06/2017. This field is only available for Complying / Term Allocated / Flexi pensions that have a start date prior to 1 July 2017.

Navigate to Fund level > Members > Browse Members > Select the relevant pension account > click Maintain Establishment Details > click Pension Details:

For most existing legacy (i.e. term allocated / complying / flexi) pensions, the 30 June 2017 special values can be entered without rolling back period update and tax finalisation.

The recorded special values will be automatically linked to these legacy pensions and included in the TBAR file, to be lodged through the tax agent portal.

For amendments in relation to the 30 June 2017 special values, you are required to update the special value in the fund in the relevant pension account then rollback and re-run the tax finalisation for 30 June 2017

Entering the 'special value' for reversionary legacy pensions

Below is a brief instruction on how to enter 'special value' for reversionary legacy pensions (i.e. term allocated / complying / flexi pensions)

- Enter the "special values" under the pension details as per above.

- Rollback 30 June 2017 tax finalisation.

- Rerun 30 June 2017 tax finalisation.

- Review TBAR records in the TBAR Console.