Issue

This article shows how Class determines a pension is a Transition to Retirement Income Stream (TRIS) in non-retirement phase and how to convert the TRIS in non-retirement phase into retirement phase once a nil cashing restriction condition of release has been met.

How Class determines that a pension is a TRIS (non-retirement phase)

Class will determine a pension account as a TRIS (non-retirement phase) based on the following factors:

- The member’s age is less than 65 and the member hasn't met a nil cashing restriction condition of release:

- Retirement

- Permanent Incapacity

- Terminal Illness

- The pension established has a condition of release of attaining preservation age, or

- The condition of release is blank for a pension account as the pension was created through a take-on process.

Class also recognises that while a TRIS (non-retirement phase) is still a type of account based pension, there are still some key restrictions:

- You cannot take your benefits as a lump sum cash payment from TRIS (unless it has unrestricted and non-preserved components)

- There is a withdrawal limit maximum of 10% of the account balance to the pension account

Resolution

This article provides the following information:

Member transitions update

Once a member has satisfied a condition of release with nil cash restriction, the TRIS can be converted to TRIS (retirement) in Class.

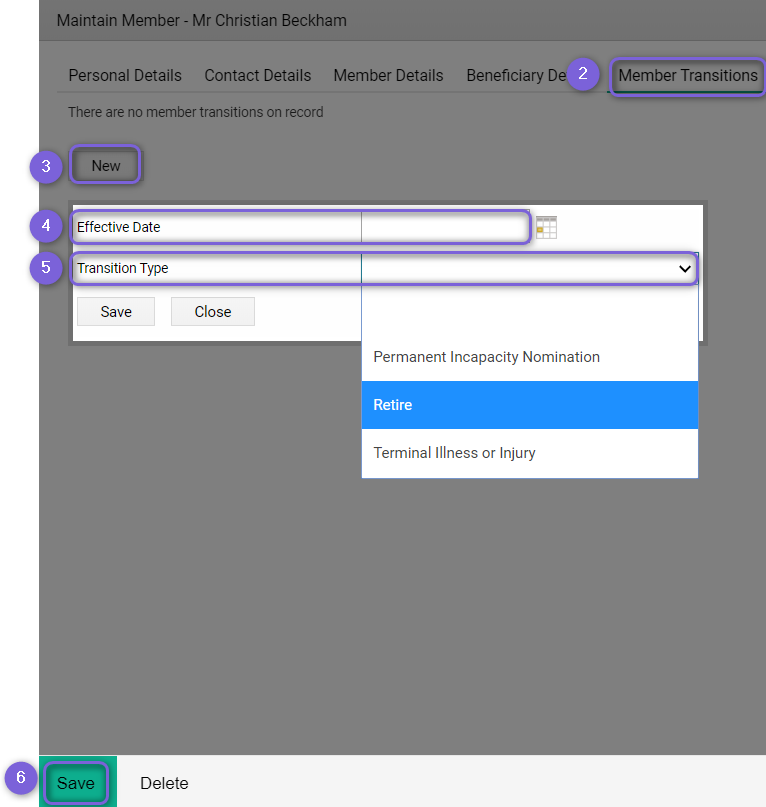

Navigate to Fund Level > Members > Browse Members

- Select the Member with the TRIS pension

- Click on the Member Transitions tab

- Click New

- Enter the Effective Date

- Select the Transition Type from the drop-down list

- Click Save

Once the Member Transition Type is in place, it effectively means the member has satisfied a condition of release with nil cash restrictions. This will shift all components to be unrestricted and non-preserved.

When the member reaches age 65, the TRIS conversion to retirement phase will happen automatically.

From 1 July 2017, when a TRIS (non-retirement) converted to TRIS (retirement), there is an additional step required, for the user to acknowledge the conversion for Transfer Balance Account Reporting (TBAR) purposes.

Refer to our User Guide for more information on TRIS Conversion.

The Effect of TRIS Conversion after 1 July 2017

|

Items |

TRIS (Non-Retirement Phase) |

TRIS (Retirement Phase) |

|

Components |

Mostly preserved |

Unrestricted and non-preserved |

|

Pension drawdown restrictions |

Maximum of 10% |

Not applicable |

|

Lump sum |

Not allowed |

Allowed |

|

Earnings |

Taxable |

Tax exempted |

|

Actuarial certificate impact |

Reduce actuarial exempt % |

Increase actuarial exempt % |

|

TBAR |

Not applicable |

Reportable |

Pension review

If the member has satisfied a nil cashing restriction condition of release, e.g. retirement during the financial year, it is recommended you do two pension reviews:

- The first pension review will start with 1 July to the date of retirement or the member’s 65th birthday.

- The second pension review will start one day after the date of retirement or member’s 65th birthday to 30 June of the financial year.

It is best practice to change the name of the account from TRIS to Account Based Pension or TRIS (Retirement).