Issue

This page explains how to process the CGT relief application event using the proportionate method and the fund chooses not to defer the capital gain (the 'non-deferral' option).

For any CGT assets in which the trustees have chosen not to defer the notional gain from deemed sale, they will be realised and included in the net capital gain for 2016/17 SMSF Annual Return. These gains will be pooled together with normal capital gains, applied against any current and prior year capital losses first, then reduced by the CGT discount, if applicable, and the 2016/17 FY pension exemption percentage.

Resolution

Navigate to Fund Level > Members > CGT relief application

Ensure the fund policy is updated with the correct actuarial percentage before processing this event.

To add a new fund policy for 2016/17 FY:

Navigate to Fund Level > Settings > Fund Defaults

- Click on Add new fund policy

- Set the start date to 1/7/2016.

'Defer Capital Gain' option is only available for funds using the proportionate method to apply for CGT relief.

- Enter the CGT Relief Date, i.e 30/06/2017

Funds using the proportionate method can only apply for CGT relief on 30/06/2017.

- Enter the Description for the event, Class defaults to "CGT Relief Application"

- Select 'No' to the 'Defer Capital Gain' radio button

- Select the parcels or investment accounts to apply for the CGT relief

- Update Parcelling (Optional)

If there are unmatched parcels arising as a result of disposals, cost base or quantity adjustments of the investment accounts, an Update button will appear in the Update Parcelling column. For any selected investment accounts that are applying for the CGT relief but have unmatched parcels, you need to click on the Update button to match the parcels first before submitting the event.

- Finalise the event

Once you have completed all relevant sections in the CGT Relief Application event, click Submit.

- Optional Step (only required for Custom Holding Account)

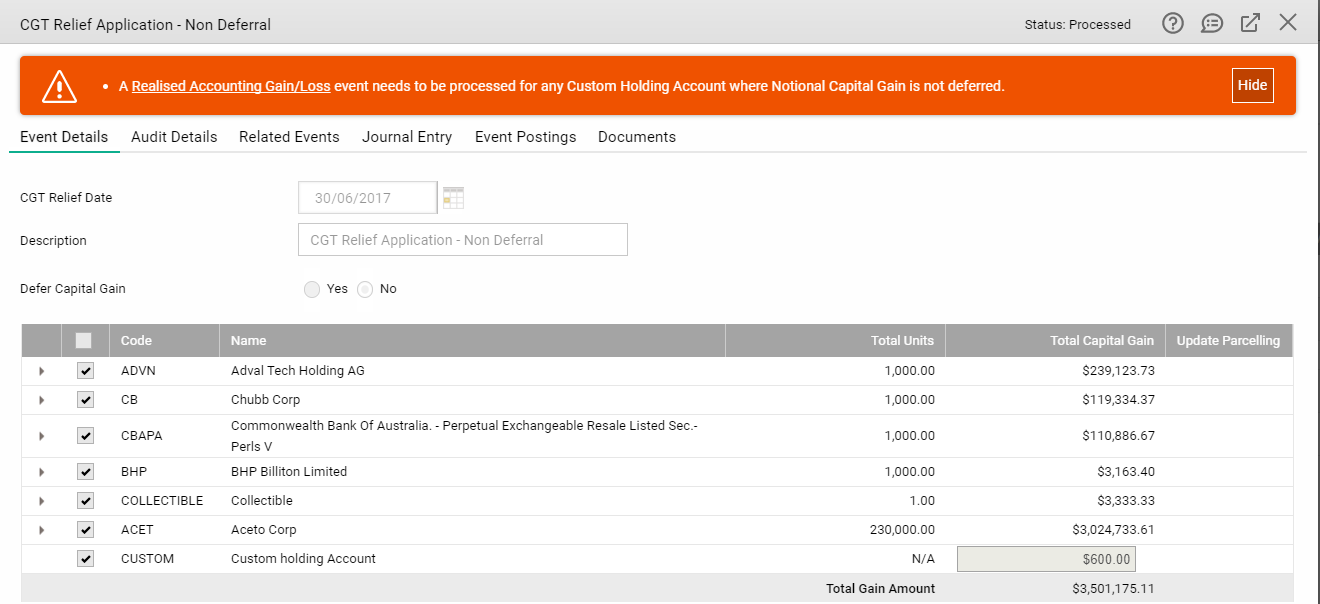

A Realised Accounting Gain/Loss event is required to be processed separately for any custom holding accounts where the notional capital gain is not deferred.

You may click on the event link showing in the warning message to navigate to this event.

For Custom Holding accounts, you should complete the realised accounting gain/loss event to ensure the capital gains tax is calculated correctly.

When not deferring the capital gains for a custom holding account, the amount recorded in CGT relief event is designed for the CGT Relief Application Minute/Resolution record keeping purpose and will not be used for the actual CGT calculation.

In the above example, the $600 is the total net capital gains (after 1/3 discount applied for any discountable gains) recognised for the Custom Holding account in 2016/17 FY and comprising of the following:

- Other Gains: $250

- Indexed Gains: $150

- Discounted Gains: $200 (Grossed up / Discountable capital gain amount is $300)

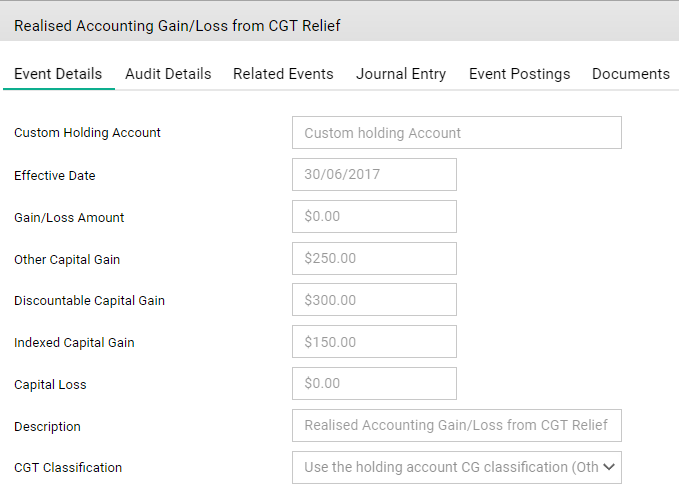

Below is the Realised Accounting Gain/Loss event worked example:

After the event is submitted, the additional information displayed in multiple tabs becomes available. Refer to our knowledge article on CGT relief application for more details.