Overview

The Class Investment Performance report has two methods of calculation, the Simple Dietz or the Modified Dietz. This page explains the method of these calculations as outlined below.

- Overview

- Simple Dietz

- Modified Dietz

- Conditions for fall back to the Simple Rate of Return

- Worked Examples

The Time-Weighted Return calculation method has been removed from the Investment Performance report. As the Time Weighted Return aims to remove the effect of the timing of flows into and out of portfolios, it does not match clients' expectations for the expected investment return of an individual holding. The Time-Weighted Return is best suited to calculate the overall portfolio return, as well as for comparisons against indices. As a result, the Time Weighted Return is still used to calculate the performance graph in our User Guide section on Client View.

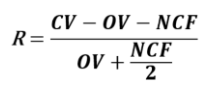

Simple Dietz

The Simple Dietz method measures the investment performance for the period based on the assumption that capital flows occur in the middle of the reporting period. The standard formula can be expressed as:

Definitions

|

Symbol |

Definition |

Notes |

|---|---|---|

|

CV |

The closing market value of the asset at the end of the reporting period. |

*If the asset does not exist at the end of the reporting period, CV = market value of the asset as of the last disposal date and this is not included in the Net Capital Flow for the period. |

|

OV |

The beginning market value of the asset at the start of the reporting period. |

*If the asset does not exist at the beginning of the reporting period, OV = the market value of the asset as of the first purchase date and this is not included in the Net Capital Flow for the period. |

|

NCF |

Net capital in- and outflow during the period. |

|

The modification also applies to the aggregated level to work out the total investment return of a group of assets based on the selected grouping method. For example, if the investments are grouped by 'Market Type', and the opening value is nil across all assets within this market type, then the acquisition value will be used as the opening value to work out the total return for this market type for the period.

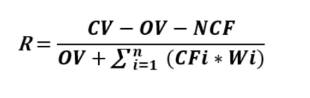

Modified Dietz

The Modified Dietz method improves on the Simple Dietz formula by taking into account the impact of the timing of any cash flows in the calculation of the investment return for a period. The standard formula can be expressed as:

Definitions

|

Symbol |

Definition |

Notes |

|---|---|---|

|

CV |

The closing market value of the asset at the end of the reporting period. |

|

|

OV |

The beginning market value of the asset at the start of the reporting period. |

|

|

NCF |

Net capital in- and outflow during the period. |

Acquisition = inflow (positive); Disposal = outflow (negative) |

|

The adjusted net cash flows, where the sum of each cash flow CFi multiplied by its weight Wi. |

|

|

|

CFi |

The net cash flow on a specific day i. |

|

|

Wi |

Cash flow adjustment factor. It is the weighting ratio to be applied to external cash flow on a specific day i, i.e. the number of days were available for investment during the period. The calculation is as follows:

TD = total number of days within the reporting period. Di = number of calendar days since the beginning of the period until the day on which the cash flow CFi occurred. Class assumes the acquisition and income flow occurs at the start of the day while the disposal flow occurs at the end of the day. |

*If the asset does not exist at the end or the beginning of the reporting period, the weighting ratio will be adjusted to reflect the number of days the asset is held within the reporting period. TD = total number of days while the asset is held within the fund during the reporting period Di = number of days since the beginning of the asset is first purchased until the day on which the cash flow occurred. Class assumes the acquisition and income flow occurs at the start of the day while the disposal flow occurs at the end of the day. *The modification also applies to the aggregated level to work out the total investment return of a group of assets based on the selected grouping method. For example, if the investments are grouped by 'Market Type', and the opening value is nil across all assets within this market type at the start of the reporting period, then Di will be adjusted to reflect the number of days since the first acquisition of the asset within this market type. |

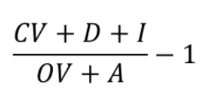

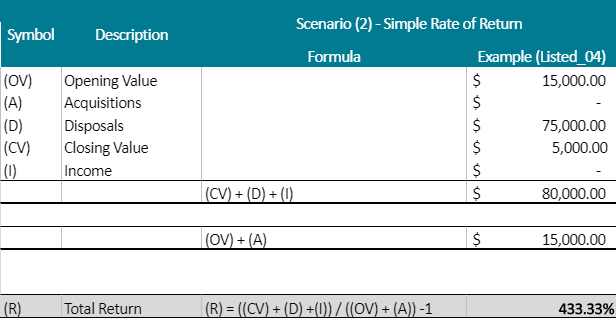

Conditions for fall back to the Simple Rate of Return

Due to issues inherent in the Simple Dietz & Modified Dietz methodology, it can produce an invalid return in circumstances of extreme intra-period asset appreciation (and realisation of these gains). If the denominator in the Dietz return calculation is either negative or zero, a Simple Rate of Return will be substituted for the affected investments. Those investments will be flagged with an asterisk and a footnote will also be displayed.

The Simple Rate of Return is calculated as follows:

Definitions

| Symbol | Definition |

|---|---|

| CV | The closing market value of the asset at the end of the reporting period. |

| OV | The beginning market value of the asset at the start of the reporting period. |

| D | Disposals |

| A | Acquisitions |

| I | Income for the reporting period |

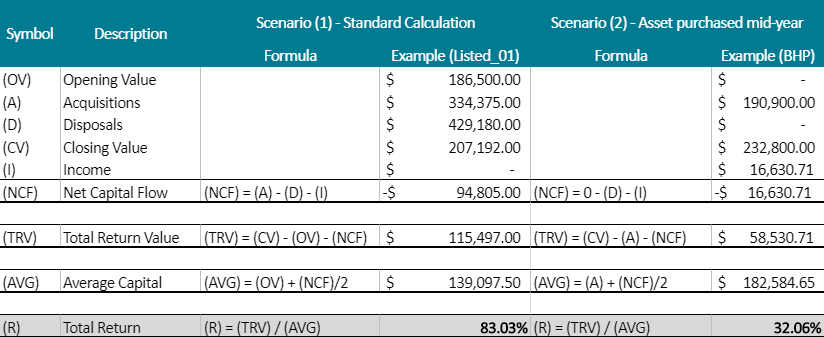

Worked Examples

Simple Dietz Calculation

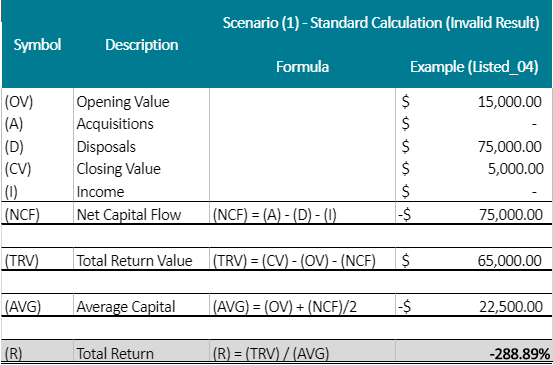

Example case where an invalid result is returned by the Simple Dietz methodology

As explained above, in some circumstances the Simple Dietz methodology returns an invalid result - an example is shown below:

In this case, a Simple Rate of Return is substituted - see the final table in this article: Simple Rate of Return calculation

Simple Rate of Return calculation

You may download the worksheet here.

Sample Document

Individual holding accounts can be removed from the calculation, please click on the relevant investment type to see how to do this refer to our User Guide sections Bank Account, term deposit, collectibles, custom holding account and property.