Issue

This page shows you how to process Pension Account Crystallisation in Class. This is where a pension with Pre 1 July 2007 ETP components is crystallised after 30 June 2007 into the new tax components (e.g. Taxable - Taxed, Tax-Free, etc.).

Prerequisites

A period update needs to be run before the crystallisation of a pension to ensure the members balance accurately reflects all current transactions.

Screen Navigation

The URLs for Accumulation Crystallisation, Pension Crystallisation and Pre-July Pension Draw-downs are hidden.

|

Event |

URL |

Comment |

|

Accumulation Crystallisation |

This event allows users to crystallise a member's ETP components into the new tax components.

|

|

|

Pension Crystallisation |

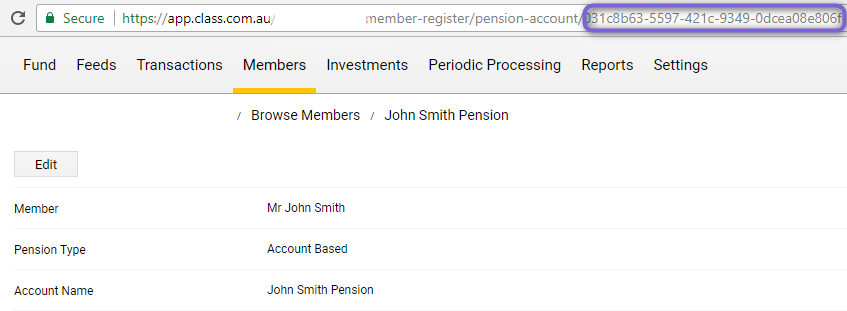

This event allows users to crystallise a pension's old ETP component into the new tax component. Replace the business code and fund code in URL. Replace the 'pension-accounting-unique-GUID' in the URL with the unique GUID for the pension account. The unique pension GUID can be accessible when you click on the pension account. Example of the URL to use:

|

|

|

Pre-July 2007 Pension Drawdowns |

This event allows users to process Pre-July 2007 Refer to help page Pension Drawdown - Pre-July 2007 for further information. |

Field Descriptions

|

Field Name |

Field Description |

Field Validation |

Example |

|

Select Member |

Member for which crystallisation is taking place. |

Mandatory drop-down field. |

Basil Fawlty. |

|

Select Pension Account |

Name of pension account from which crystallisation is taking place. Only the applicable pension accounts will be available to select. |

Mandatory drop-down field. |

Basil's Pension. |

|

Crystallisation Date |

Crystallisation date of pension. |

Mandatory date field. |

01/07/2017 |

|

Last Period Update |

Last date that period update is run to. |

Mandatory protected date field. |

01/07/2017 |

|

Last Period Review |

The latest date of a period review for the select pension account. |

Mandatory protected date field. |

01/07/2017 |

|

Taxable Proportion |

The Taxable Proportion of the selected pension account after crystallisation. |

Mandatory protected field. No data entry is required. |

0.5000 |

|

Description |

Description for the pension crystallisation event. |

Mandatory free text field. |

Pension Account Crystallisation |

Submitting Pension Account Crystallisation

Once the required data has been entered, the pension crystallisation can be submitted. Click the Submit button.

Income Streams Started by July 2017

A super interest, where at least one income stream benefit was paid before 1 July 2007, is valued and proportioned once a trigger event occurs. Until a trigger event occurs, the tax-free component continues to be worked out using the deductible amount that was applied to the benefit before the law changes came into effect.

Trigger events

There are four events that will trigger a change in the way you work out tax-free and taxable component:

- if the member was 60 years old or older on 1 July 2007

- when the member turns 60 years old

- when the member dies

- when the income stream is partially or wholly commuted.

While it is unlikely, there may still be some instances where an income stream has not already been subject to a trigger event since 1 July 2007, for example:

- disability income stream benefits

- death benefit income streams paid to a non-dependant (payments to a dependant are tax-free, so the proportions do not need to be calculated).

For a super income stream paid from an untaxed source, the only possible trigger event is commutation. This is because the legislation provides that the trigger event of turning 60 and the death of the person who is the holder of the super interest only apply where there is no untaxed element.

When a trigger event occurs, the value of the super income stream interest and the tax-free component of the super interest are calculated at the time just before the trigger event occurred. If there are two or more trigger events, the tax-free component is determined at the time just before the earliest of those events.

When a trigger event occurs, the tax-free and taxable components are calculated as:

- tax-free component = the total of the unused undeducted purchase price + the pre-July 1983 component

- taxable component = the value of the super interest less the tax-free component.

If the income stream started before 1 July 1994, a pre-July 1983 component is not added.

The tax-free and taxable components of all future income stream benefits paid after the trigger event will be paid using the same proportions as those that make up the total value of the super interest supporting the income stream just before the trigger event.

Crystallisation Deadline: 30 June 2008

By this date super fund trustees, including trustees of Self Managed Superannuation Funds, must have calculated the crystallised segment of all superannuation interests in the Fund.

An administrative penalty of 5 units will be imposed for each breach of this requirement. Superannuation providers that do not ensure this date calculate this amount may be subject to a penalty of up to $850.

The crystallised segment only applies to superannuation interests which commenced before 1 July 2007. The crystallised segment represents (subject to one exception) that portion of the superannuation interest which relates to the period before 1 July 2007.