Issue

How do I process the Unibail takeover of WFD Corporate Action manually?

Resolution

To manually process the Corporate Action:

- Download the ATO calculator

- Record the acquisition details of the WFD holdings

- Create and activate the URW account in the fund

- For the proportion that attracts CGT rollover relief, process Spin off / Demerger

- For the proportion that CGT rollover doesn’t apply, process the acquisition of URW with the units and cost base calculated accordingly with CGT date 7 June 2018

- Process disposal of WFD on 7 June 2018 with the cost base proportion that is not eligible to receive CGT Rollover Relief (from step 4) PLUS the cash consideration received

Worked Example

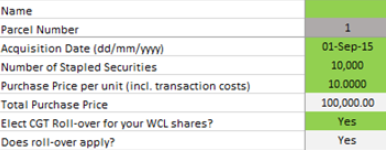

The fund holds 10,000 units (at $10 each) of WFD that was originally acquired on 1 Sep 2015.

Download the ATO calculator

Record the acquisition details of the WFD holdings

The below screenshot is an example

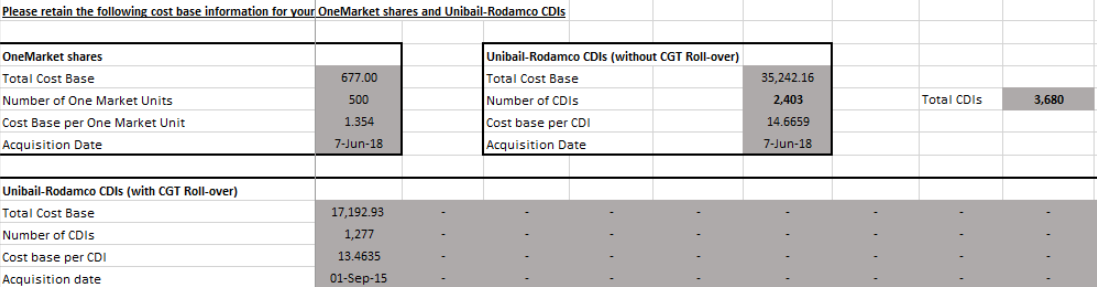

Based on whether the rollover relief can be applied, you will see the URW CDIs will be separately displayed in two sections, one without CGT roll-over relief and the other with CGT roll-over relief.

Create and activate the URW account in the fund

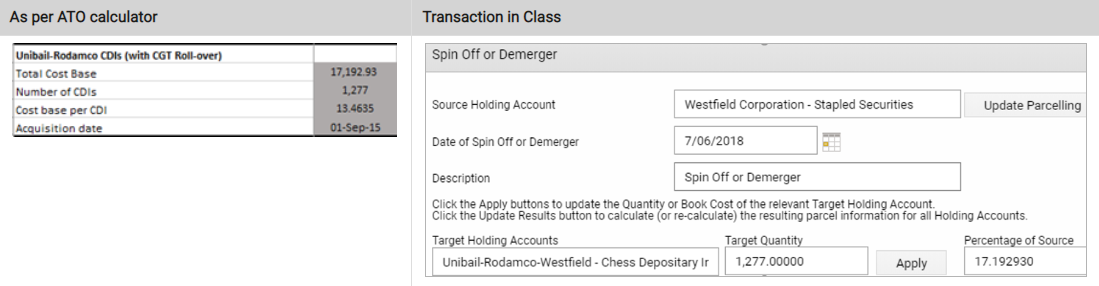

For the proportion that attracts CGT rollover relief, process Spin off / Demerger

Navigate to Fund Level > Transactions > Investment - Corporate Action > Spinoff or Demerger

The percentage of source is worked out based on the total cost base in URW displayed in the calculator divided by total original cost base of the WFD shares, $17,192.93 / $100,000 = 17.19293% and this portion will become the cost base in URW CDIs.

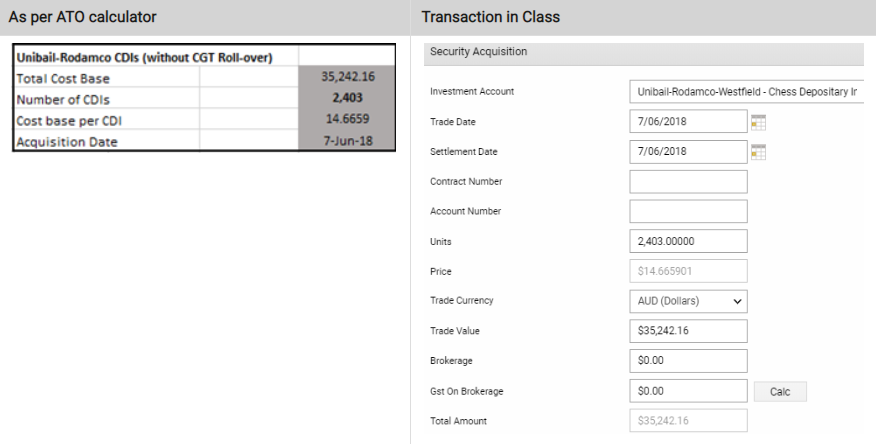

For the proportion that CGT rollover doesn’t apply, process the acquisition of URW with the units and cost base calculated accordingly with CGT date 7 June 2018

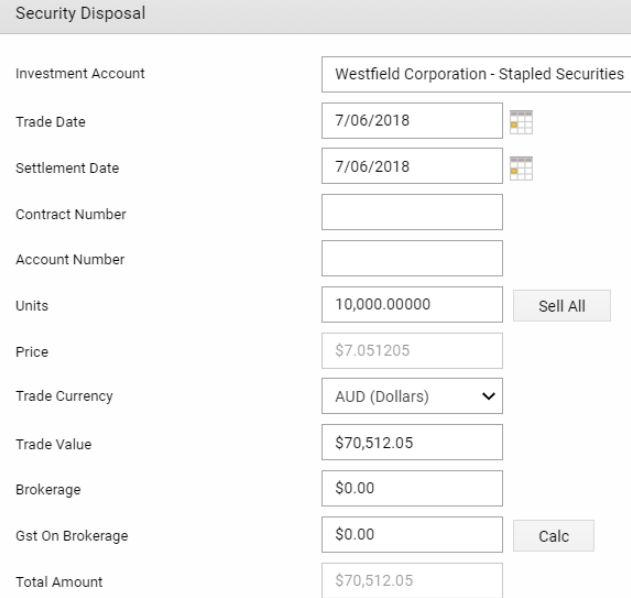

Process disposal of WFD on 7 June 2018 with the cost base proportion that is not eligible to receive CGT Rollover Relief (from step 4) PLUS the cash consideration received.

Compute the following which makes up of the disposal consideration:

- The URW scrip value that was received in exchange of the WFD. This is the same amount as stated in step 4, $35,242.16.

- Cash consideration is equal to $3.51536 per units of the original WFD held. This is calculated as: $3.51536 * 10,000 = $35,153.60.

- There will be an additional cash proceed paid for the fractional entitlement of the URW Stapled Security resulting from the rounding prior to the CDI allocation at the rate of $14.53716297. In this example, the investor would have received 3,688 (10,000 * 0.01844 * 20) URW CDIs but only received 3,680 URW CDIs due to the rounding rule. An additional cash proceed will be paid for the 8 units and computed as: 8 * $14.53716297 = $116.29, rounded down to the nearest whole cents.

The total capital proceed of WFD disposal is then calculated as: (a) $35,242.16 + (b) $35,153.60 + (c) $116.29 = $70,512.05.

Once the transaction is processed, match the transaction with Step 4 and two lots of cash received from the bank. This will calculate the capital gain and losses from the disposal.

- Due to the complexity around this transaction, the following steps are only recommended if the fund only holds one parcel of WFD and WFD has not participated in the 2017 transitional CGT relief.

- The ATO calculator assumes that you haven't processed the previous Westfield Restructure and you have processed all the tax deferred amounts exactly based on the tax deferred allocations the group has made. If either of these is not true, the cost base split proportion and the capital gains or loss result in Class won't match exactly with the ATO calculator.