Introduction

This page provides illustrative worked examples to process the recent Westfield Corporation (WFD) Stapled Securities restructure in Class.

General Disclaimer: Any information expressed in this page does not purport to be any financial or tax advice as we have not taken into account any of your financial or tax objectives that are specific to your circumstance. While effort has been made to make sure the information is as accurate and relevant as possible, it should be construed as general information to assist Class users in understanding the implications of the corporate action. You should not rely on the information provided as advice, instead seek your own independent advice from appropriately qualified practitioners or conduct your own research.

Specific Disclaimer:

You should NOT use the automated Corporate Action for the following scenarios:

- If the fund records WFD in 3 separate investments, i.e. Westfield American Trust (WAT), WFD Trust (WFDT) and Westfield Corporation Limited (WCL).

- If the fund holds 108 or less WFD securities at the time of the 2018 Westfield Restructure. The fund would be defined as a Minimum Holder and would have received cash instead of Unibail-Rodamco CDIs. You are required to process the Unibail takeover transaction manually via a disposal event.

- If there are any WFD parcels with CGT date prior to 17 July 2004. The system does not support the Unibail takeover transaction and you are required to process the transaction manually.

- If a data feed has created any transactions that relate to this Westfield Corporate Action in the fund. You should consider deleting those transactions and process with the automated Corporate Action provided by Class or process it manually to ensure cost base changes are handled appropriately.

Important Information on using the ATO's Westfield Calculator

- When entering parcels into the ATO's calculator, for any parcels of WFD prior to 30 June 2014 and 20 December 2010, you must enter the original cost base for WDC (as if the previous two Westfield restructures were never processed), not the reduced cost of WFD; as the ATO's Westfield Calculator attempts to reconstruct both 2010 and 2014 restructure.

- Tax deferred adjustment amount built into the ATO's Westfield calculator may differ to the actual tax deferred amount processed in Class, hence result in differences in the capital gains or losses calculation between Class and the ATO.

- For any parcels of WFD that is less than 55 units, Class currently does not allow the parcel to participate in rollover relief as 54 x 0.0184 = 0.9936 < 1 whole unit of URW stapled shares. As such the allocation of URW CDI for rollover relief portion and non rollover relief portion may differ slightly due to rounding errors.

- There may be small discrepancies between the Class template and the ATO's calculator due to the difference in rounding practice.

Case Study 1: No Rollover Relief

Case Facts:

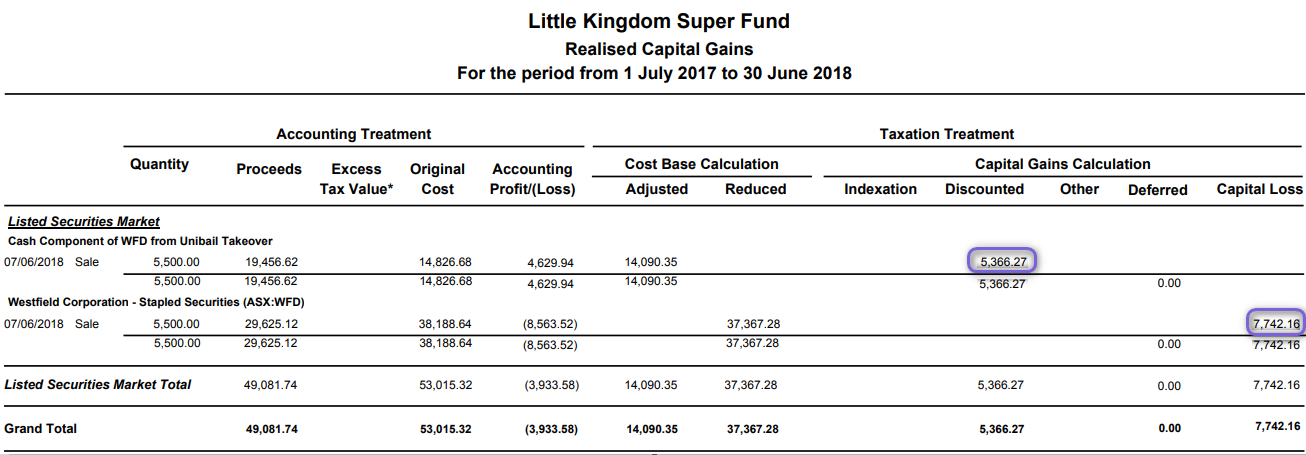

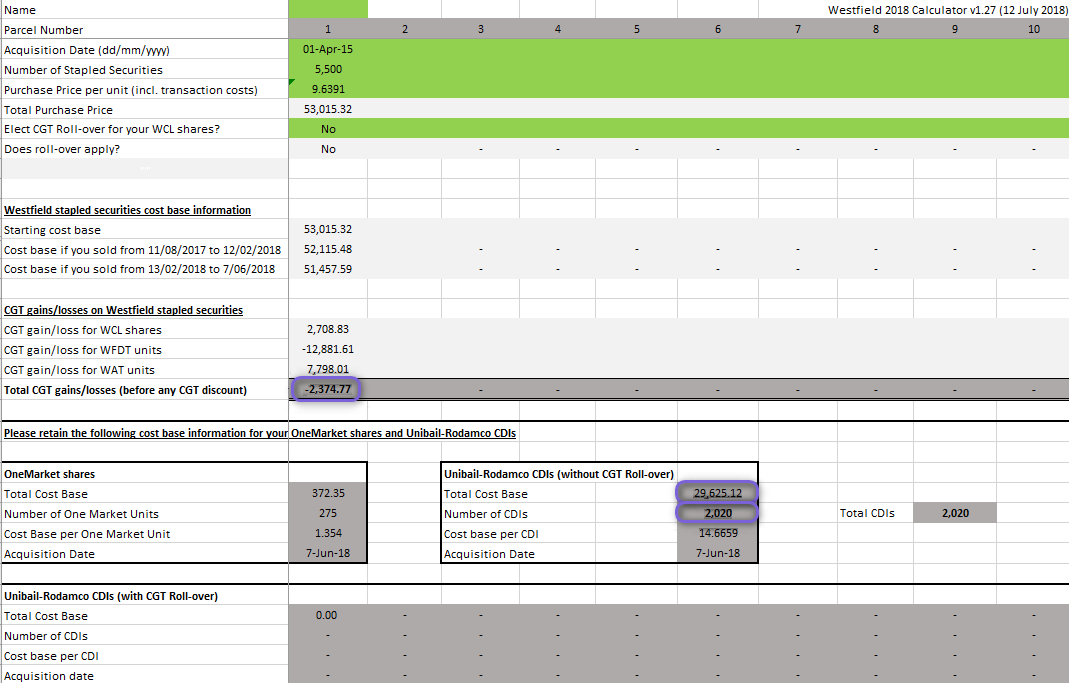

Little Kingdom Super Fund currently owned 5,500 units of Westfield Corporation - Stapled Securities (WFD), which were purchased on 1/4/2015 for $53,015.32.

Step 1: Demerger of OneMarket

0.0677 x 5,500 = $372.35 (unfranked Dividend)

This in-specie distribution will be the cost base of OMN: 5,500 / 20 = 275 units.

Optional Step: Ben and Holly Kingdom, as the trustees of the fund, elected to sell the OMN (< 500 units) through the sale facility: Process a sale of 275 @ $1.5113= $316.56. This should be matched with the cash received on 22 June 2018.

Step 2: Enter WFD 2018 Annual Tax Statement

Ensure the Distribution Tax Statement event for WFD is entered with effective date as at 7/6/2018, and tax deferred amounts of $0.194084 x 5,500 = 1,067.46

Step 3: Spin-off Cash Component of WFD > URW

Cash Component = 3.515365 x 5,500 = $19,334.51

And Fractional Entitlement (5500 x 0.01844 - 101) x 20 = 8.4 (URW CDI) @ $14.53716297 = $122.11

Total Cash = $19,456.62

Step 4: Takeover of WFD > URW using Scrip Component

5,500 x 0.01844 x 20 = 101 x 20 = 2,020 units of URW CDI @ VWAP of $14.6659 = $29,625.12

Check Reports:

- Realised Capital Gains Report: $7,742.16 - $5,366.27 = $2,375.89 (Capital Losses)

- Unrealised Gains Report:

- Check ATO's calculator:

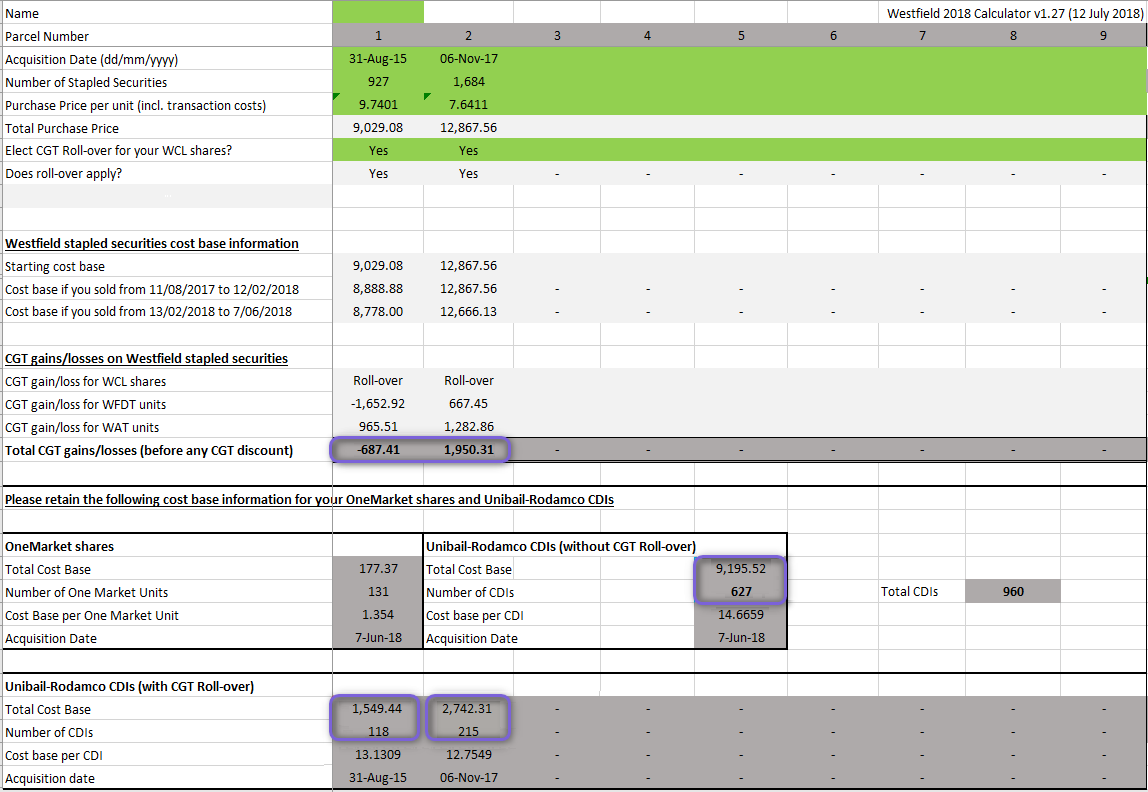

Case Study 2: With Rollover Relief

Case Facts:

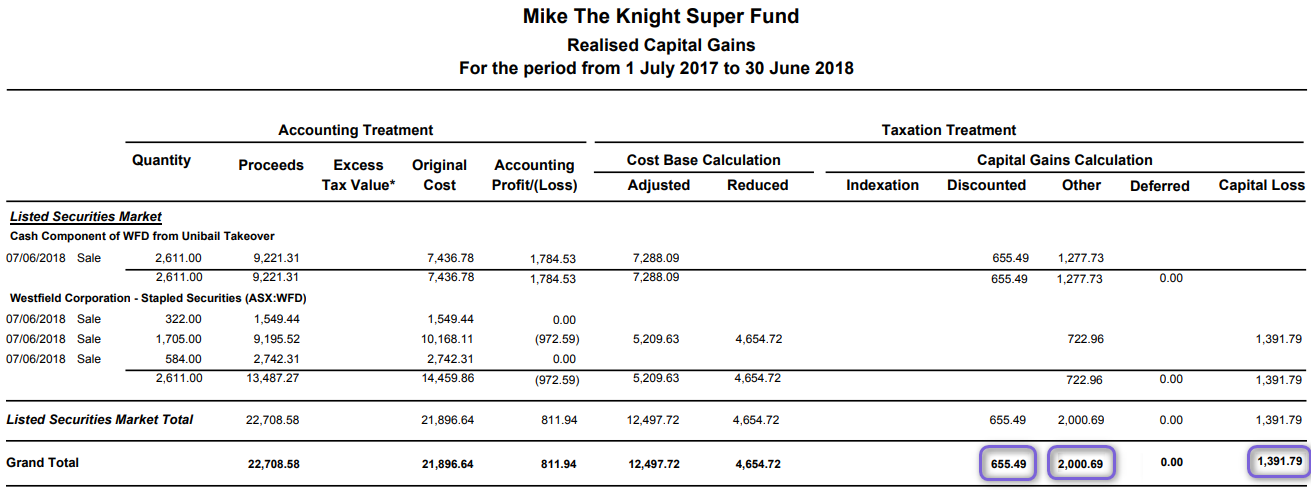

Mike The Knight Super Fund currently owned two parcels of Westfield Corporation - Stapled Securities (WFD).

|

Parcel

|

Purchase Date

|

Units

|

Cost Base

|

Cumulative Tax Deferred

|

|---|---|---|---|---|

| 1 | 927 | $9,029.08 | $71.13 | |

| 2 | 1,684 | $12,867.56 | N/A |

Step 1: Demerger of OneMarket

0.0677 x (927+1,684) = $176.76 (unfranked Dividend)

This in-specie distribution will be reinvested into OMN: (927+1,684) / 20 = 131 units.

Optional Step: Mike Knight, as the trustee of the fund, elected to sell the OMN (< 500 units) through the sale facility: Process a sale of 131 @ $1.5113= $197.98. This should be matched with the cash received on 22 June 2018.

Step 2: Enter WFD 2018 annual Tax Statement

Ensure the Distribution Tax Statement event for WFD is entered with effective date as at 7/6/2018, and tax deferred amounts agree with the actual statement: 927 x (0.0267+0.0477) + (927 + 1684) x (0.1076+0.012) = $381.32

Step 3: Spin-off Cash Component of WFD > URW

Cash Component = 3.515365 x (927+1684) = $9,178.62

And Fractional Entitlement ((9276+1684) x 0.01844 - 48) x 20 = 2.9368 (URW CDI) @ $14.53716297 = $42.69

Total Cash = $9,221.31

Step 4: Takeover of WFD > URW using Scrip Component

(927+1684) x 0.01844 x 20 = 48 x 20 = 960 units of URW CDI

The ATO accepts that the portion of the Unibail-Rodamco shares that were received in respect of your WCL shares was 34.7% and the portion that were not received in respect of your WCL shares was 65.3%.

|

Parcel

|

Purchase Date

|

Units

|

Rollover Relief Units

|

Non Rollover Relief Units

|

|---|---|---|---|---|

| 1 | 927 | 927 x 34.7% / 2611 x 960 = 118 | 927 x 65.3% / 2611 x 960 = 223 | |

| 2 | 1,684 | 1,684 x 34.7% / 2611 x 960 = 215 | 1,684 x 65.3% / 2611 x 960 = 404 | |

| Total | 118 + 215 = 333 | 223 + 404 = 627 |

Check Reports:

- Realised Capital Gains Report: $655.49 + $2,000.69 - $1,391.79 = $1264.39 (Capital Gain)

- Unrealised Gains Report:

- Check ATO's Calculator: -687.41 + 1950.31 = $1262.90 (Capital Gain)

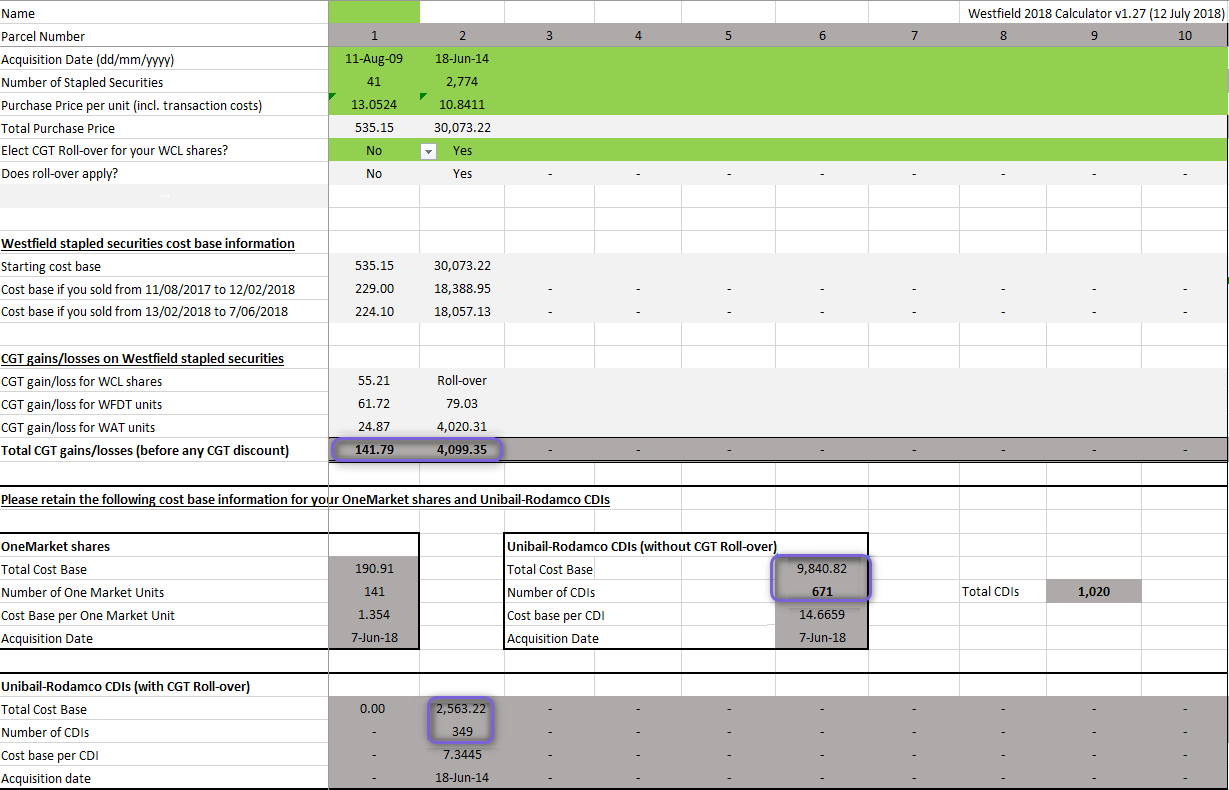

Case Study 3: Pre 20 Dec 2010 and Pre 30 Jun 2014 Parcels

Case Facts:

Piggy Family Super Fund currently owned Westfield Group Stapled Securities (WDC), which has gone through 2010 restructure to create Westfield Retain Trust (WRT) and 2014 restructure to merge with WRT to form Scentre Group (SCG).

Westfield Group Stapled Securities (WDC)

|

Parcel

|

Purchase Date

|

Units

|

Cost Base

|

Cumulative Tax Deferred

|

2010 Restructure

|

|---|---|---|---|---|---|

| 1 | 41 | $535.15 | $38.63 (Up to 30 June 2013) | $117.26 (or 41% of Westfield Trust) cost base transferred into WRT | |

| 2 |

|

2,774 | $30,073.22 | N/A | N/A |

On 30 June 2014, WDC was restructured again and became Westfield Corporation Stapled Securities (WFD).

|

Parcel

|

Purchase Date

|

Units

|

Cost Base

|

Cumulative Tax Deferred

|

2014 Restructure

|

|---|---|---|---|---|---|

| 1 | 41 | $535.15 - $117.26 - $148.77 = $269.12 | $46.45 (Up to 30 June 2017) | $148.77 (or 26.3% of Westfield Holding Limited and 46.7% of Westfiled Trust) cost base transferred into Scentre Group (SCG). | |

| 2 |

|

2,774 | $30,073.22 - $10,706.07 = $19,367.15 | $528.99 (Up to 30 June 2017) | $10,706.07 (or 26.3% of Westfield Holding Limited and 46.7% of Westfiled Trust) cost base transferred into Scentre Group (SCG). |

Step 1: Demerger of OneMarket

0.0677 x (41+2,774) = $190.58 (unfranked Dividend)

This in-specie distribution will be reinvested into OMN : (41+2,774) / 20 = 141 units.

Optional Step: Poppy Pig, as the trustee of the fund, elected to sell the OMN (< 500 units) through the sale facility: Process a sale of 141 @ $1.5113= $213.09. This should be matched with the cash received on 22 June 2018.

Step 2: Enter WFD 2018 annual Tax Statement

Ensure the Distribution Tax Statement event for WFD is entered with effective date as at 7/6/2018, and tax deferred amounts agree with the actual statement: = $0.194084 x 2,815= $546.33

Step 3: Spin-off Cash Component of WFD > URW

Cash Component = 3.515365 x (41+2,774) = $9,895.75

And Fractional Entitlement ( 2,815 x 0.01844 - 51) x 20 = 18.172 (URW CDI) @ $14.53716297 = $264.17

Total Cash = $10,159.92

Step 4: Takeover of WFD > URW using Scrip Component

(41+2,774) x 0.01844 = 51 x 20 = 1,020 units of URW CDI.

The ATO accepts that the portion of the Unibail-Rodamco shares that were received in respect of your WCL shares was 34.7% and the portion that were not received in respect of your WCL shares was 65.3%.

|

Parcel |

Purchase Date |

Units |

Rollover Relief Units |

Non Rollover Relief Units |

|

1 |

31 Aug 2009 |

41 |

If the parcel units is < 55, Class will not allow it to receive rollover relief |

41 x 0.01844 x 20 = 15 |

|

2 |

06 Nov 2016 |

2774 |

34.7% x (1020-15) =349 |

65.3% x (1,020 - 15) = 656 |

|

|

|

Total |

349 |

671 |

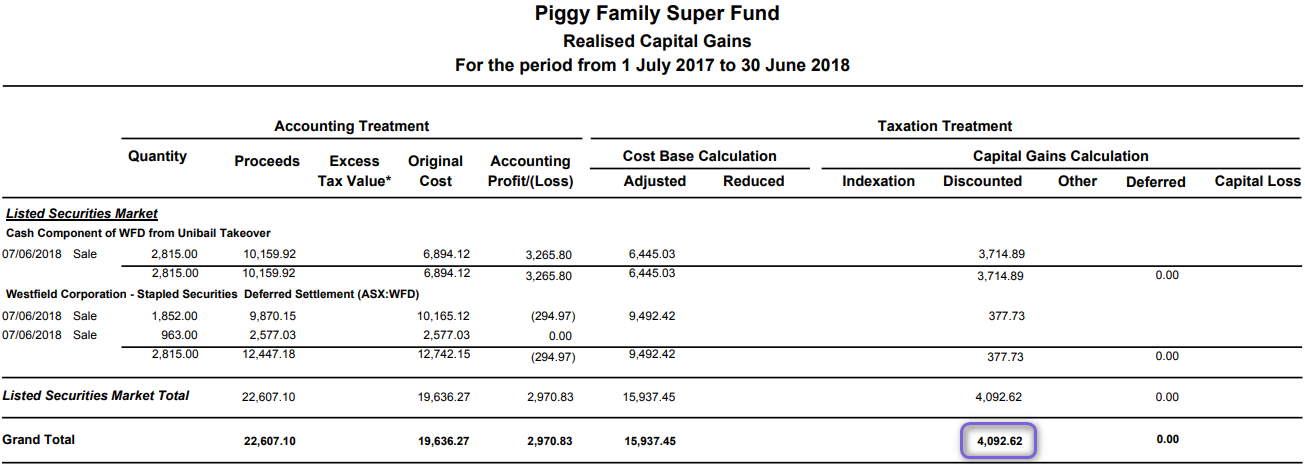

Check Reports:

- Realised Capital Gains Report: $4,092.62 (Discounted Capital Gain)

- Unrealised Gains Report:

- Check against ATO's Calculator:

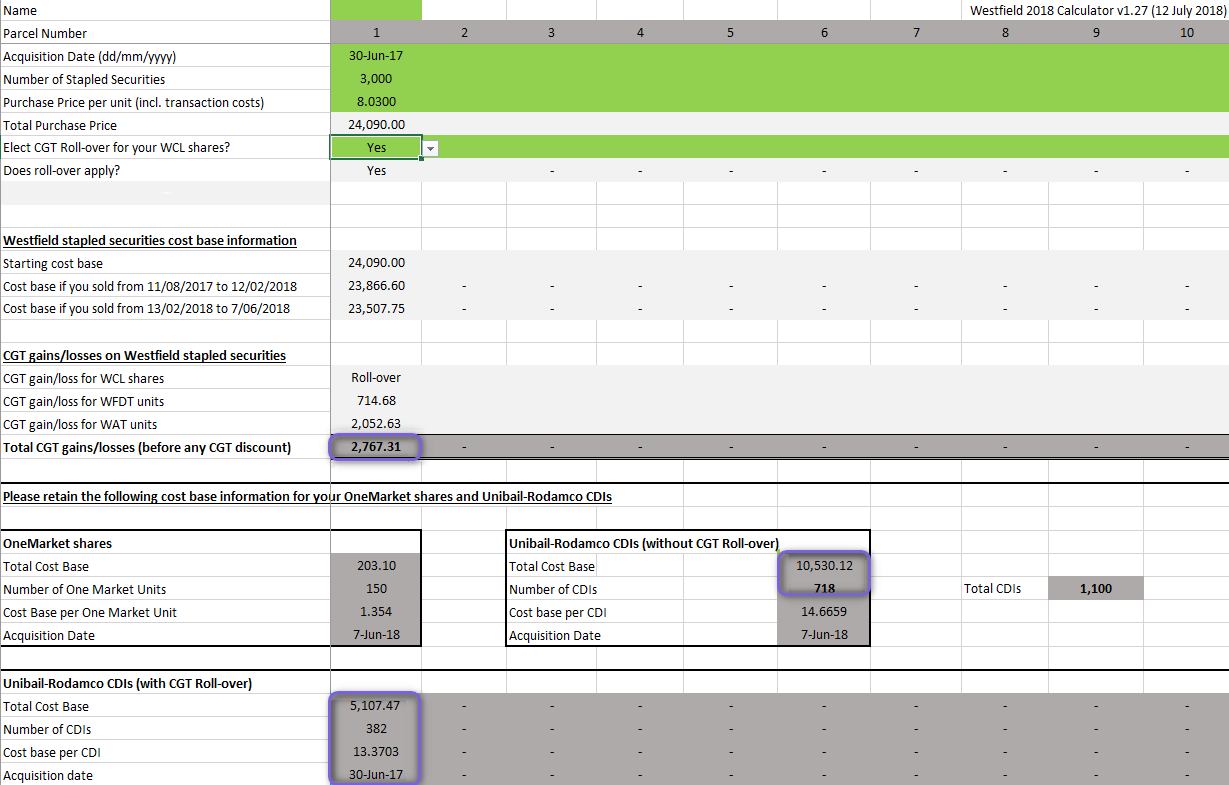

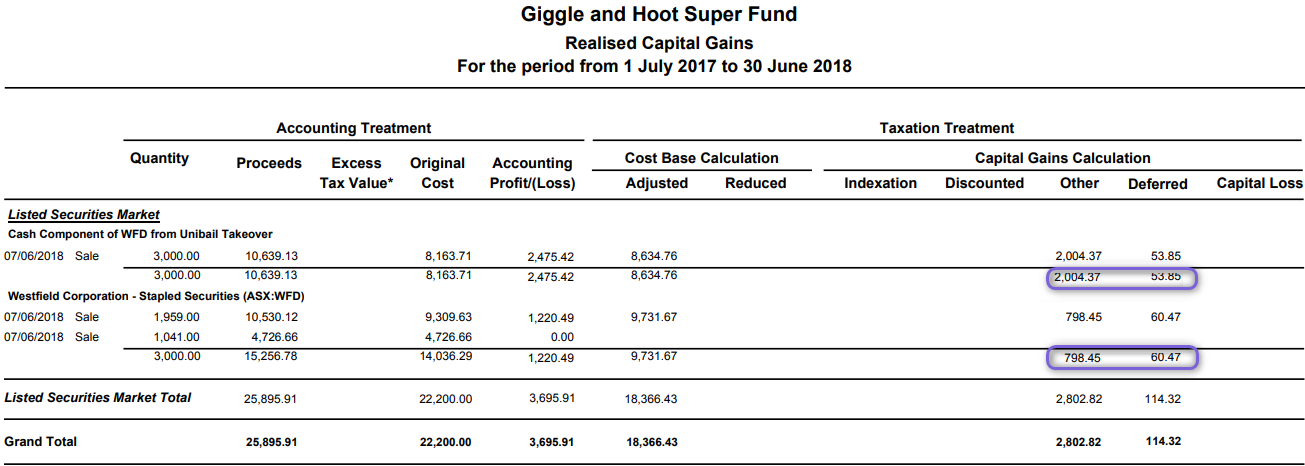

Case Study 4: Transitional CGT Relief + Partial Rollover Relief

Case Facts:

Giggle Family Super Fund currently purchased 3,000 units of Westfield Corporation - Stapled Securities (WFD) on 15/7/2014 for $22,200. On 30 June 2017, the fund elected to take Transitional CGT relief, and reset its cost base to $8.03 per unit.

|

Parcel

|

Purchase Date

|

Units

|

Cost Base

|

Cumulative Tax Deferred

|

CGT Relief Cost Base Adjustment

|

Deferred Notional Gains

|

|---|---|---|---|---|---|---|

| 1 |

|

3,000 | $22,200 | $552.360 (Up to 30 June 2016) | $24,090 - $22,200 = $1,890 | ($24090- ($22,200 - $552.36))x 2/3 x (1-91.006%)= $146.45 |

Step 1: Demerger of OneMarket

0.0677 x 3,000 = $203.10 (unfranked Dividend)

This in-specie distribution will be reinvested into OMN: 3,000 / 20 = 150 units.

Step 2: Enter WFD 2018 annual Tax Statement

Ensure the Distribution Tax Statement event for WFD is entered with effective date as at 7/6/2018, and tax deferred amounts of: $0.194084 x 5=3,000 = $582.25

Step 3: Spin-off Cash Component of WFD > URW

Cash Component = 3.515365 x 3,000 = $10546.09

And Fractional Entitlement (3,000 x 0.01844 - 55) x 20 = 6.4 (URW CDI) @ $14.53716297 = $93.04

Total Cash = $10,639.13

|

Items

|

Description

|

WCL

|

WFDT

|

WAT

|

Total

|

|---|---|---|---|---|---|

| (a) | NTA as at 30 June 2017 (Appendix A: NTA Table) | 20.25% | 47.53% | 32.22% | 100.00% |

| (b) | Accounting Cost Base ($22,000 x NTA %) | $4,495.50 | $10,551.66 | $7,152.84 | $22,200.00 |

| (c) | CGT Relief Cost Base Adjustment ($1,890 x NTA%) | $382.73 | $898.32 | $608.96 | $1,890.00 |

| (d) | Unadjusted Tax Cost ($24,090 x NTA%) | $4,878.23 | $11,449.98 | $7,761.80 | $24,090.00 |

| (e) | Tax Deferred per Unit (Appendix B: Tax Deferred Table) | 0.1343502 | 0.0597340 | 0.1940842 | |

| (f) | Tax Deferred (Tax Deferred CPU x 3,000 / 100) | 403.05 | 179.20 | 582.25 | |

| (g) | Cash Component of the Consideration Per Unit | $0.5485 | $2.9668 | $3.5153 | |

| (h) | Scrip Component of the Consideration Per Unit | $1.7919 | $3.3720 | $0.2449 | $5.4088 |

| (i) | Total Consideration Per Unit | $1.7919 | $3.9205 | $3.2117 | $8.9214 |

| (j) | Accounting Cost Base - Cash Component: (b)x(g)/(i) | N/A | $1,476.30 | $6,607.42 | $8,083.72 |

| (k) | CGT Relief Cost Base Adjustment - Cash Component: (c)x(g)/(i) | $125.68 | $562.52 | $688.20 | |

| (l) | Unadjusted Tax Cost Base - Cash Component: (j) + (k) | $1,601.98 | $7,169.94 | $8,771.92 | |

| (m) | Tax Deferred - Cash Component: (f)x(g)/(i) | $56.39 | $165.54 | $221.93 | |

| (n) | Adjusted Tax Cost Base - Cash Component: (l) - (m) | $1,545.59 | $7,004.40 | $8,549.99 | |

| (o) | Deferred Notional Gains Realised - Cash Component: (j)/$22,200 x $146.45 | $9.74 | $43.59 | $53.33 | |

| (p) | Cash Consideration - Cash Component: ($3.51536472 x 3,000) | $1,645.59 | $8,900.51 | $10,546.09 | |

| (q) | Accounting Gain - Cash Component: (p) - (j) | $169.29 | $2,293.09 | $2,462.37 | |

| (r) | Capital Gain - Cash Component: (p) - (m) | $100.00 | $1,896.11 |

$1,996.10 |

Fractional Entitlement Calculation: $93.04 / $14.53716297 = 6.4 (URW CDI); 6.4 / 20 / 0.01844 = 17 units WFD.

|

Items

|

Description

|

Amount

|

TOTAL (Cash Component + Fractional Entitlement) |

|---|---|---|---|

| (L) | Deferred Notional Gains Realised - Fractional Entitlement: ($146.45 - (o)) x (17/3000) | $0.53 | $53.33+ $0.53 = $53.86 |

| (E) | Tax Deferred - Fractional Entitlement: ($582.25 - (l)) x (17/3000) | $2.04 | $221.93 + $2.04 = $223.97 |

| (C) |

CGT Relief Tax Adjustment - Fractional Entitlement: (1,890 - (k)) x (17/3000) |

$6.81 | $688.20 + $6.81 = $695.01 |

| (K) | Capital Gain - Fractional Entitlement: (I) - (F) | $8.28 | $1,996.10 + $8.28 = $2,004.38 |

| (J) | Accounting Gain - Fractional Entitlement: (I) - (B) | $13.05 | $2,462.37 + $13.05 = $2,475.42 |

| (B) |

Accounting Cost Base - Fractional Entitlement: (22,200-(j)) x (17/3000) |

$79.99 | $8083.72 + $79.99 = $8,163.71 |

| (F) | Adjusted Tax Cost Base - Fractional Entitlement: (D) - (E) | $84.76 |

$8,549.99 + $84.76 = $8,634.75 |

| (D) |

Unadjusted Tax Cost Base - Fractional Entitlement: (l) + (D) |

$86.80 | $8,771.92 + $86.80 = $8,858.72 |

| (I) | Cash Consideration - Fractional Entitlement | $93.04 | $10,546.09 + $93.04 = $10,639.13 |

| (A) | Residual Units - WFD | 17 | |

| (G) | Fractional Entitlement Equivalent in URW CDI | 6.4 | |

| (H) | Consideration Per Unit - Fractional Entitlement | $14.53716297 |

Step 4: Takeover of WFD > URW using Scrip Component

3,000 x 0.01844 x 20 = 55 x 20 = 1,100 units of URW CDI.

|

Parcel

|

Purchase Date

|

Units/ Amount

|

Rollover Relief Units

|

Non Rollover Relief Units

|

|---|---|---|---|---|

| 1 | 1100 | 34.7% x 1,100 =382 | 65.3% x `1,100 = 718 | |

| Deferred Notional Gains | $146.45 - $53.86 = $92.59 | 34.7% x $92.59 =$32.13 | 65.3% x $92.59 = $60.46 |

Check Reports:

- Check Realised Gains Report

- Check Unrealised Gains Report

- Check against ATO's Calculator