This article will guide you through the process of amending and adjusting the allocation of profit/losses and tax among members or member accounts.

Navigate to Fund Level > Periodic Processing > Period Updates and select the relevant financial year

- Select the period update link which requires amending

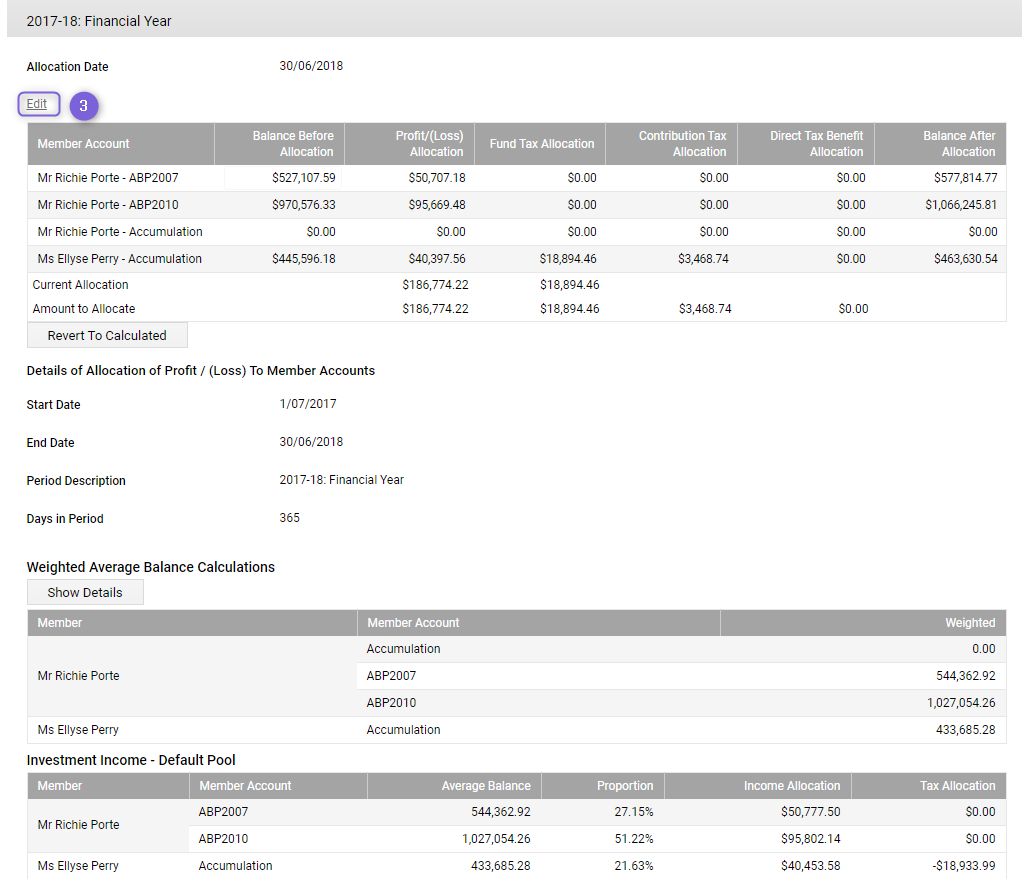

- Select the Allocate Benefits to Members. The following screen will appear displaying the allocation of profit/loss and tax, and the basis on which these amounts have been calculated

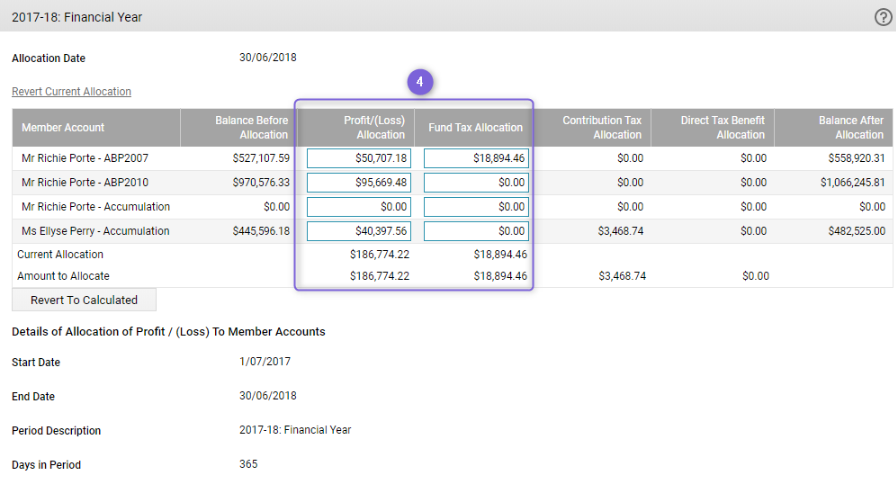

- Select Edit to adjust the profit/loss and tax allocation

- You will now be able to edit the allocation of the Profit/(Loss) Allocation and Fund Tax Allocation only by typing in the fields. Amend the allocated amounts as required

- Click Save

Ensure that the total Current Allocation amount entered equals to the total Amount to Allocate, otherwise the change will not be accepted.

The Contribution Tax Allocation and Direct Tax Benefit Allocation cannot be amended as they result from direct member events such as Contributions and Member Insurance Premiums.

You can also increase or decrease Profit/(Loss) Allocation and Fund Tax Allocation for the same magnitude, provided the net position remains the same.

You can always use the Revert to Calculated button to undo any changes to the allocation that you have made. This will revert the figures back to the system calculated allocation.

Period Updates

The following should be noted regarding how Class' Period Update works:

- Class allocates profit/loss and tax based on the member's weighted average balance

- Class does not generally allocate any tax expenses to pension accounts, except for the share of franking credits which will be displayed as a tax benefit

- Class allocates tax to the accumulation accounts up to the point where the allocation equals the profit/loss amount associated with given income/expense transactions. Any balance is again allocated to the accumulation accounts proportionately until exhausted. In the event that there are no remaining accumulation balances, the allocation will revert to pension accounts on a proportionate basis to prevent negative accumulation balances

- Fund Level Expenses by default are always apportioned using the Fund Expense Exemption %, even if it is paid from a bank account that is segregated for pension purposes. Paying an amount of money will reduce the benefits of the segregated pool to the pension accounts, but it does not determine the deductibility of the expense. This is because most fund expenses cannot be separated (except for investment expenses related to investment assets segregated for pension accounts), actuarial fee, auditor fee, accountancy fee, supervisory levy, general interest charge and so on.

Frequently Asked Questions

How is the allocation of benefit to members computed?

There are two parts to the calculation of benefits to be allocated to a member's account.

- The investment income / (loss), which is computed as:

Total investment income $ xxx

add: Total investment gain xxx

Total $ xxx

less: Investment-related expenses

Bank fees xx

Non-deductible exp xx

Total investment income / (loss) $ xxx - The fund level income, which is computed as:

Other income $ xxx

less: fund expenses (except investment related expenses in #1 above) xxx

Fund level income / (loss) $ xxx

All of this is then distributed using the weighted average balance of the member. You can view this under the Allocate Benefit to Member screen:

How does Class calculate the residual tax?

The residual tax is calculated by the following:

Income Tax Expense (includes provision for deferred tax if you track tax effect accounting, otherwise it will be tax effect on taxable income)

Less Contribution Tax

Less Direct Member Expense

Less Tax Allocation from Investment Income

Less Tax Allocation from fund Income

What's Next?

Learn how to run a Period Update & Lodging an Annual Return